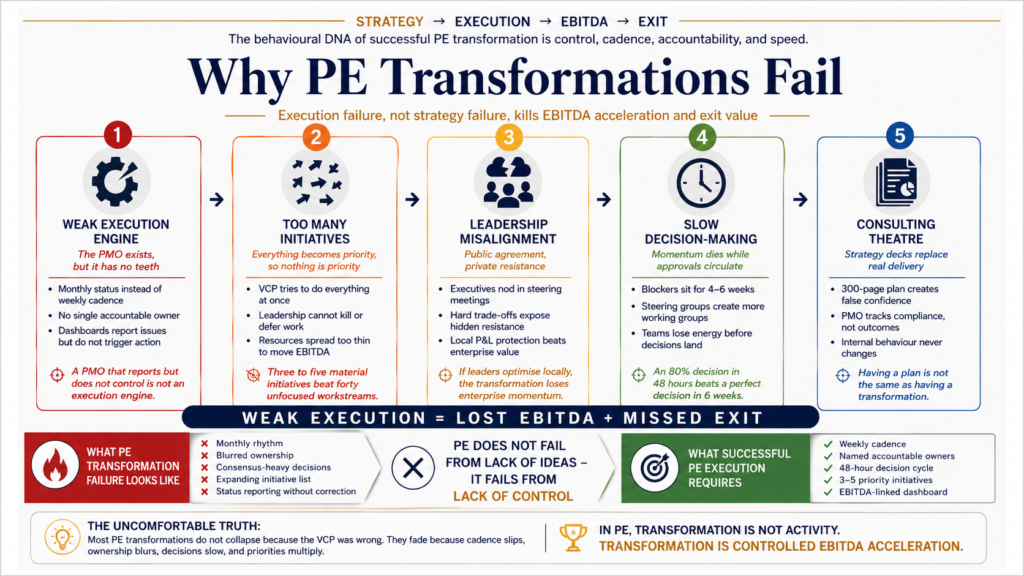

Why Most PE Transformations Fail (And No One Talks About It)

The Uncomfortable Truth About Execution, Not Strategy Private Equity doesn’t fail because of bad strategy. It fails when execution never becomes controlled, measurable, and real. Everyone celebrates PE transformation stories. You hear them at conferences, in case studies, on LinkedIn. The ones where a struggling business gets acquired, undergoes a dramatic transformation, and emerges leaner, faster, and worth 3–5x more than the entry price. McKinsey publishes studies on transformation success rates. Bain publishes frameworks for managing change at scale. Harvard Business Review runs features on how enterprises successfully navigated digital transformation. What you don’t hear are the quiet ones. The transformations that stopped halfway through. The ones where momentum died at month 4. The initiatives that looked perfect on a 100-day plan but collapsed under the weight of operational reality. The promised EBITDA that never materialised. The exit window closed because the business hadn’t actually changed. Based on 30 years in transformation programmes — at scale, across industries, in high-stakes environments — I’ve seen enough of these failures to know they follow a pattern. I’ve worked through post-acquisition integrations at Fortune 500 firms. I’ve run PMOs on nine-figure transformation programmes. I’ve been brought in as a turnaround officer to salvage transformations that were already failing. I’ve also been the sponsor on the PE side, looking at a struggling portfolio company and asking the hard question: why hasn’t this changed? And here’s what nobody wants to say out loud, because it’s uncomfortable and it implicates every leader who’s been through this: Most PE transformations fail not because the strategy was wrong. They fail because the execution engine never became real. The Five Silent Killers When a PE-backed transformation falters, it’s almost always one of these five things. Not all at once — but usually at least two, working together to kill momentum. What’s insidious about these failures is that they don’t manifest as dramatic breakdowns. They manifest as a slow drift. As a creeping scope. As initiatives that are technically ‘on track’ but aren’t delivering the needle-moving results they were supposed to. 1. Weak Execution Engine (The PMO That Isn’t) Here’s the dangerous assumption that disabled people make most transformations: if you build the right plan, execution will follow. It won’t. The most common transformation failure I’ve seen is a PMO that looks good on the org chart but doesn’t actually drive anything. It has meetings. It has workstreams. It has a 200-page roadmap with Gantt charts and resource allocations. It has governance tiers and escalation paths. It reports weekly status to steering committees. But it doesn’t have teeth. A weak execution engine typically exhibits these symptoms: Monthly status updates instead of weekly cadence. Transformation momentum requires constant visibility. In a monthly steering committee, too much can go wrong between meetings. Blockers that should be cleared in 2 days sit for 3 weeks. Small misses compound into big ones. A monthly rhythm is basically an admission that you’re not managing by fact — you’re managing by hope and hoping the next month’s update is better than this month’s. No single point of accountability. When a workstream misses a milestone, who owns it? If the answer isn’t crystal clear — one name, one person, one P&L — then it’s everyone’s responsibility, which in practice means nobody’s. I watched a transformation workstream on supply chain efficiency miss three successive milestones before anyone acknowledged it wasn’t happening. Seven people were listed as ‘sponsors’ for the initiative. Decisions deferred to consensus. I’ve watched transformations grind to a halt because the PMO couldn’t make a $2M decision without five rounds of stakeholder consultation. There’s an appeal to consensus — it feels inclusive. It feels safe. But by the time consensus forms across five business units with competing interests, the market has moved, and the initiative is already behind. Dashboards that don’t drive behaviour. You can have all the red/amber/green metrics you want. If they don’t lead to immediate corrective action — if a red metric doesn’t trigger an emergency decision meeting within 48 hours — then you’re just producing status reports dressed up as KPIs. The dashboard serves as a cover: ‘We tracked it closely,’ the PMO says, even though nothing actually changed in response. PMO focused on process instead of outcomes. The most dangerous transformation of PMO is one that confuses process compliance with delivery. ‘All workstreams submitted their risk registers.’ ‘Governance tiers are in place.’ ‘Change management plan is complete.’ These are process boxes. They’re not EBITDA. A transformation PMO’s job isn’t to ensure the process is perfect — it’s to ensure the business changes. The PE firms that succeed insist on a fundamentally different operating model for the execution engine. Weekly cadence — not monthly. Unambiguous ownership — one person’s name next to each initiative. Escalation paths that clear decisions in 48 hours, not 6 weeks. Dashboards that trigger action, not just reporting. An execution engine isn’t a support function — it’s the organism that keeps the transformation moving. 2. Too Many Initiatives, Zero Prioritisation A classic mistake in transformation planning: the first Value Creation Plan tries to do everything, because everything represents an opportunity. Improve margins through aggressive cost reduction across all functions. Drive growth through channel expansion, product innovation, and geographic rollout. Modernise the technology infrastructure and migrate to the cloud. Restructure talent and eliminate redundancy. Get exit-ready by creating sustainable, scalable operations. Improve customer experience and NPS. Refine the go-to-market strategy. All simultaneously. The result: thousands of people working across dozens of workstreams, nothing delivered with real impact. Small wins scattered across initiatives, but no material EBITDA impact. Teams are exhausted by complexity and context switching. Leadership is confused about what actually matters. I was brought in to salvage a transformation at a mid-market manufacturer that was struggling. The company had been PE-backed for 18 months. The transformation had identified over 40 initiatives across cost, revenue, technology, and organisational restructuring. Every business unit was running three to four ‘high-priority’ programmes. Nobody had time to focus on anything. And EBITDA

The New Transformation PMO

From Project Tracking to Enterprise Value Delivery Executive Summary: Why This Matters Now If you are a CIO, CTO, or transformation leader, you are facing a reality your predecessors never encountered: simultaneous, parallel execution of transformations that would have been sequential in earlier eras. Your organisation is likely managing: AI adoption and capability building; ERP system modernisation; cloud migration across hundreds of applications; cybersecurity hardening and resilience programmes; data platform development; digital channel transformation; regulatory compliance and control frameworks; and cost optimisation initiatives. All at the same time. All are competing for the same engineering talent, budget, executive attention, and vendor resources. All are carrying real organisational risk. The traditional PMO—built for a simpler era when organisations ran discrete, sequential projects—is not designed for this environment. It produces status reports that no one acts on. It identifies risks that stakeholders have already accepted. It tracks milestones that feel increasingly disconnected from business outcomes. It often optimises for schedule and budget adherence while transformation programmes deliver little value, achieve poor adoption, or create new operational risks that are not measured. The organisations that are winning—those delivering real business value from their transformations—operate a fundamentally different model. Their PMO is not a reporting office. It is an enterprise value engine. This article explores what that means, why it matters, and how to build it. Why Project Tracking Alone Is Not Enough Traditional PMOs emerged in the 1990s and 2000s when enterprises ran projects sequentially. Build an ERP system. Migrate to the cloud. Deploy a data warehouse. Each project had a clear scope, defined end date, and measurable success criteria. A PMO that tracked progress, escalated risks, and controlled scope was genuinely valuable. That world no longer exists. Modern transformation is not sequential—it is parallel and continuous. A bank cannot wait to finish one digital platform before beginning another. An enterprise cannot modernise its ERP system in isolation from its cloud strategy, data infrastructure, or cybersecurity posture. The dependencies are too complex. The pace of change is too fast. The organisational risk is too high. When a traditional PMO focuses purely on schedule and budget tracking, it becomes a bureaucratic cost centre in this environment. It produces documents that no one acts on. It identifies risks that stakeholders have already accepted. It escalates issues at a pace that prevents timely decision-making. Worse, it often optimises for completion metrics—on-time delivery, budget variance—without asking whether the finished project is actually being adopted, creating business outcomes, or generating the benefits promised to investors. Real value delivery requires a PMO that operates at three distinct levels: strategically (aligning transformation to business objectives), operationally (managing execution, reducing friction, coordinating delivery), and financially (tracking benefits realisation and return on investment). A PMO that does only one or two of these is incomplete and will underperform. Connecting Strategy to Execution: The Critical Role The most critical role of a modern PMO is to bridge the gap between enterprise strategy and programme execution. This sounds straightforward, but it is remarkably rare in practice. Most organisations have strategies and execution plans that operate in separate domains. The board approves a digital transformation strategy. Finance approves a portfolio of projects. Operations manages delivery. Three years later, the execution has little to do with the original strategy, and no one can explain why. A value-delivery PMO changes this dynamic. It starts by translating strategy into concrete terms. What does “ become a digital-first organisation” actually mean in terms of architecture, capability, investment, and risk? What outcomes should the business expect from each major programme? What trade-offs is leadership willing to accept? What measures will we use to know we succeeded? What dependencies exist between programmes? With strategy translated into measurable objectives, the PMO then ensures that every programme is aligned to these outcomes. This requires a sophisticated portfolio management capability: understanding not just what each programme does, but how it contributes to strategic goals, how it interacts with other programmes, what shared capabilities it depends on, and where critical sequencing exists. It also requires the PMO to take an active—not passive—role in governance. Too many PMOs are silent observers. They report status. A value-delivery PMO actively shapes decisions. When two programmes compete for scarce engineering resources, the PMO helps leaders make the call based on strategic priority and risk exposure. When a vendor is underperforming and jeopardising other initiatives, the PMO escalates the issue and proposes solutions. When benefits are not being realised because the business is not adopting the new platform, the PMO identifies the barrier and drives corrective action. Portfolio Complexity: The New Normal Portfolio complexity in modern enterprises has reached unprecedented levels. Consider a typical scenario: These are not sequential. They overlap. They compete for resources. They create dependencies that can derail one another if not carefully managed. Traditional project management approaches fail at this scale. You cannot schedule 20 parallel programmes as a single waterfall plan. You cannot manage dependencies by meeting coordination alone. You need intelligent portfolio orchestration: a single source of truth about what is planned, what is in flight, what has finished, and what is creating bottlenecks or risk. This level of visibility enables leaders to sequence initiatives in ways that maximise strategic value while managing risk, prevents the common failure mode in which programmes are approved independently with no one managing the cumulative load, and helps make hard choices about prioritisation based on strategic alignment, resource availability, and expected benefits. Vendor and Partner Governance: A Major Source of Failure A significant source of transformation failure is the weak governance of vendors and partners. Modern transformations depend on external partners: systems integrators, software vendors, managed service providers, niche specialists, and consulting firms. Poor vendor governance is a primary driver of cost overruns, schedule delays, quality issues, and benefit shortfalls. Common failure modes include unclear scope definition and change control; weak accountability for partner performance; poor integration of partner delivery into overall programme governance; misaligned incentives between vendor and customer; inadequate oversight of vendor subcontractors; and failure

Cyber Resilience Must Now Move at Machine Speed: A Strategic Imperative for 2026

Executive Summary Cybersecurity and cyber resilience are not the same. Cybersecurity protects systems. Cyber resilience protects the business. As artificial intelligence, machine-speed threats, and sophisticated ransomware campaigns accelerate, organisations must fundamentally shift how they think about cyber risk—from a technical problem to a business continuity imperative. According to the World Economic Forum’s 2026 Cybersecurity Outlook, cyber-enabled fraud, phishing, ransomware, and AI vulnerabilities have become top executive concerns. Recent strategic partnerships between the UAE and industry leaders like IBM and Palo Alto Networks underscore a critical insight: trusted AI and national cyber resilience are now inseparable from digital sovereignty and economic competitiveness. For CIOs, CTOs, and technology leaders, this convergence creates both an urgent challenge and a strategic opportunity. Organisations that embed resilience into their operating model, governance structures, and leadership accountability will outcompete those that treat cyber as a technical compliance exercise. Part 1: The Strategic Context The Threat Landscape is Accelerating The cyber threat landscape of 2026 is fundamentally different from that of even three years ago. Threats are not just more numerous—they are faster, more intelligent, and more destructive. AI-Enabled Attacks: Threat actors are now using machine learning to identify vulnerabilities, craft targeted phishing campaigns, and exploit weaknesses at scale. A human security analyst might take days to identify a pattern of compromise. An AI-powered attack can propagate across networks in hours. Ransomware as a Business: Ransomware is no longer opportunistic. It is now a sophisticated criminal enterprise with operational disciplines, negotiating tactics, and supply chains. Major ransomware gangs have budgets in the tens of millions of dollars and employ security researchers to discover zero-day vulnerabilities before defenders know they exist. Supply Chain Weaponisation: Attackers increasingly target the ecosystem—vendors, contractors, managed service providers—to reach their ultimate target. A compromise of a single managed service provider can affect hundreds of downstream customers simultaneously. Insider Risk Amplified: As remote work becomes normalised, the insider threat surface has expanded. Employees with access to critical systems are no longer confined to corporate offices, where their behaviour can be monitored. Insider threats—whether malicious or negligent—are now one of the fastest-growing sources of breaches. Critical Infrastructure Targeting: Attacks on operational technology, industrial control systems, and critical infrastructure are increasing. These attacks often move slowly, conducting reconnaissance for weeks or months before launching a disruptive event. A successful attack on a utility, transportation system, or healthcare facility can affect millions of people. The World Economic Forum’s 2026 Cybersecurity Outlook captures this acceleration. When surveyed, executives cite AI-enabled fraud and ransomware as their top two concerns—not because these are new threats, but because both have become dramatically more effective and difficult to defend against. Why Speed Now Matters In previous generations, cyber incidents unfolded over days or weeks. A breach was detected, investigated, contained, and remediated over a period that allowed for deliberate decision-making and communication. That timeline no longer exists. Modern ransomware can encrypt terabytes of data in hours. A compromised credential can enable lateral movement within a network in minutes. An AI-powered attack can spawn variations faster than a human security team can respond. This speed imperative changes everything about how organisations must be structured to respond to cyber incidents. If your incident response process requires escalation through multiple approval layers, meetings to coordinate response, and formal change management procedures, you will be unable to respond fast enough to modern threats. By the time you have assembled the decision-makers, the attack will have accomplished its objective. Cyber resilience in 2026 requires automation, clear decision rights, pre-authorised response playbooks, and the ability to activate recovery procedures without waiting for normal business processes to take their course. The UAE Context: Digital Sovereignty and Strategic Resilience The UAE’s strategic emphasis on cyber resilience reflects a broader regional understanding: digital trust and cyber resilience are foundational to economic growth and digital sovereignty. Recent partnerships between the UAE government and global cybersecurity leaders such as IBM and Palo Alto Networks are not merely procurement arrangements. They represent a strategic commitment to build capabilities, governance frameworks, and institutional knowledge that position the region as a leader in trusted AI and cyber resilience. For enterprises operating in the UAE and broader GCC region, this creates both expectations and opportunities: Regulatory Evolution: As governments invest in cyber resilience, regulatory frameworks will follow. Organisations that embed resilience practices early will find themselves ahead of compliance curves. Those who wait for mandates will face costly retrofitting. Vendor Assessment Rigour: As governments establish partnerships with trusted security vendors, enterprise procurement processes will increasingly require assessments of cyber resilience maturity. Vendors that cannot demonstrate resilience capabilities will face friction in the market. Thought Leadership Opportunity: Technology leaders who position themselves as experts in cyber resilience—not just cybersecurity—will gain a competitive advantage in executive recruitment and board-level influence. This is a moment when CIOs and CTOs can elevate from “IT operations” to “business continuity strategy.” International Credibility: For enterprises seeking to expand beyond the region, demonstrating compliance with UAE/GCC cyber resilience standards becomes a competitive advantage. It signals maturity to international partners and customers. Part 2: Bridging the Gap Between Cybersecurity and Cyber Resilience The Distinction Cybersecurity is the practice of protecting systems from unauthorised access, modification, or destruction. It focuses on prevention, detection, and response to cyber attacks. Cybersecurity asks: Can we stop the attack? Can we identify it quickly? Can we limit the damage? Cyber Resilience is the capacity of an organisation to continue functioning during and after a cyber incident. It encompasses not just security controls, but operational redundancy, recovery capabilities, governance structures, decision-making authority, and stakeholder communication. Cyber resilience asks: Can the business continue to operate? Can we restore critical services? Can we maintain trust with customers and stakeholders? The two are related but distinct. An organisation can have strong cybersecurity (advanced firewalls, EDR systems, threat intelligence) and still lack resilience if it hasn’t thought through how to operate when those security controls fail—and they will fail, eventually. Why the Distinction Matters Consider a scenario: A large financial services firm has invested

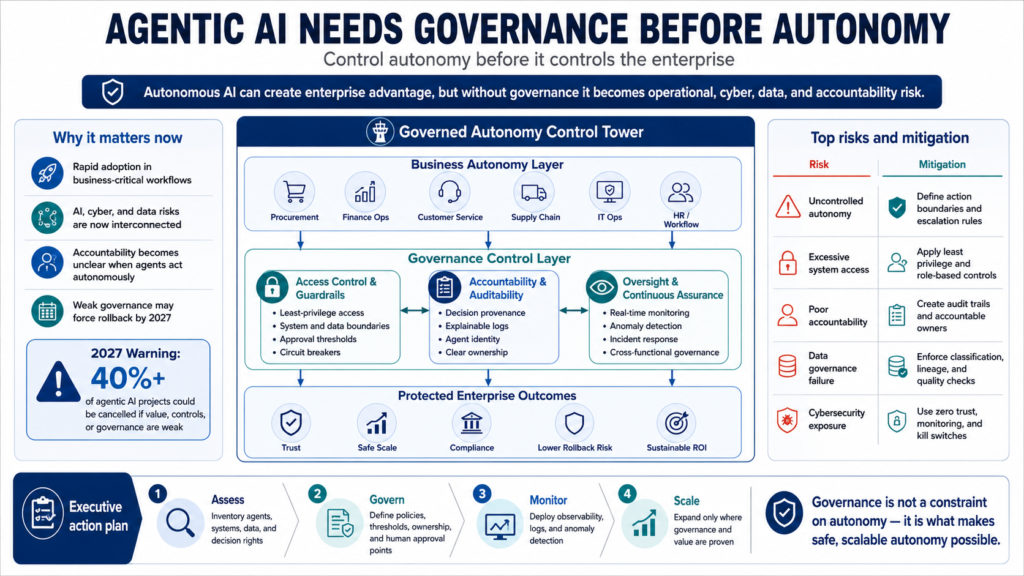

Agentic AI Needs Governance Before Autonomy: Why Enterprises Must Act Now

The promise of agentic AI is compelling—autonomous agents that learn, decide, and act with minimal human intervention. Yet as enterprises rush to deploy these systems, a critical oversight threatens to unwind years of digital transformation investment: most organisations are building autonomous AI capabilities without the governance guardrails required to operate them safely at scale. This is not a theoretical problem. Industry research increasingly points to a sobering reality: enterprises may be forced to roll back autonomous AI agents by 2027 if governance, access control, and accountability mechanisms remain weak. For CIOs, CDOs, and enterprise technology leaders, the message is clear: the window to implement governance frameworks is now, before autonomy becomes the default and control becomes nearly impossible to retrofit. The Urgency: Why Now Agentic AI has crossed a threshold. What was once a research concern has become an enterprise priority. Unlike traditional AI systems that require explicit human prompting and decision-making, agentic AI operates differently—it sets goals, takes actions, and iterates without waiting for human approval at each step. This shift is powerful but introduces a class of risks that many organisations are not yet equipped to manage. Three converging pressures make governance urgent: 1. Rapid Adoption Without Precedent Organisations are deploying autonomous agents into business-critical processes—procurement workflows, financial operations, customer service decisions, and supply chain optimisation. The speed of deployment has outpaced the maturity of governance practices. Unlike the gradual adoption of traditional AI, agentic AI is moving from pilot to production in months, not years. 2. Interconnected Risk Domains CIO priority research reveals a critical insight: operationalising AI, cybersecurity, and data strategy are now inseparable. Agentic AI systems that operate autonomously become both a vector for cybersecurity threats and a potential source of data governance violations. A compromised agent can execute decisions across systems with minimal oversight. A data governance failure becomes amplified when an agent acts autonomously on data that should have been restricted. 3. Accountability Vacuum Traditional AI operates with clear decision trails—a model scores a loan application, and a human approves it. Agentic AI operates differently. An autonomous agent decides to modify supplier contracts, reprioritise resources, or escalate customer issues. When something goes wrong, the question “who is responsible?” becomes genuinely difficult to answer. Without clear governance, enterprises risk creating systems they cannot control, debug, or defend. The 2027 Rollback Risk Gartner-linked reporting suggests a troubling scenario: many enterprises deploying autonomous agents today without robust governance frameworks will face a choice by 2027—either significantly constrain the agents’ autonomy or discontinue them entirely. This would represent a costly reversal, involving: The enterprises that avoid this scenario will be those that establish governance frameworks early—before agents become deeply embedded in operations, before stakeholder expectations are set around autonomous decision-making, and before the technical debt of ungoverned systems becomes unmanageable. The Governance Imperative: Three Pillars Effective agentic AI governance rests on three interconnected pillars: 1. Access Control and Guardrails Agentic AI systems must operate within defined boundaries. This means: 2. Accountability and Auditability Every autonomous decision must leave a clear trace. Organizations need: 3. Governance Process and Oversight Governance is not a static policy—it must evolve as agents learn and as organisations discover edge cases: The CIO Perspective: Leadership Imperatives For CIOs and technology leaders, agentic AI governance presents a distinct challenge: it sits at the intersection of technology capability, business risk, and organisational control. Three imperatives stand out: First, own governance before business leaders’ own AI deployment. If CIOs wait for business units to deploy autonomous agents and then mandate governance, the cost of retrofit will be prohibitive. Governance frameworks must be in place before agents are trained and operationalised. Second, integrate AI governance with existing control frameworks. Agentic AI governance should not be a separate track. It must integrate with cybersecurity, data governance, and operational risk management. This requires CIOs to break down silos between teams that historically have not worked together. Third, invest in observability and control infrastructure now. Managing autonomous systems requires different tooling than managing traditional systems. CIOs need to budget for and build capabilities that provide real-time visibility into agent behaviour, enable rapid rollback, and support forensic analysis when things go wrong. The Broader Stakes The stakes of getting agentic AI governance right extend beyond risk management. Organisations that establish governance frameworks early will be able to: Conversely, organisations that treat governance as a post-deployment concern will find themselves constrained by their own ungoverned systems, unable to scale what should be a competitive advantage. The Path Forward The agentic AI governance challenge is urgent but solvable. Organisations that want to harness the power of autonomous AI without ceding control should: Conclusion Agentic AI represents a genuine advance in AI capability—the ability to deploy systems that can work autonomously, learn from their experience, and improve their own performance. This is powerful. But power without governance is dangerous. The enterprises that will thrive in an agentic AI future are those that recognise governance not as a constraint on autonomy but as the foundation for it—the mechanism that makes safe, scaled, sustainable autonomous AI possible. The 2027 rollback scenario is not inevitable. It is a warning. Organisations that act now to establish governance frameworks, integrate them with existing control structures, and maintain human oversight of autonomous systems will be positioned to compete in an age of agentic AI. Those that do not will find themselves managing the legacy costs of ungoverned autonomy—or abandoning autonomous systems altogether. The time to act is now, before autonomy becomes the default. Before governance becomes the bottleneck. Before rolling back becomes the only option. #AgenticAI #AIGovernance #CIO #DigitalTransformation #Cybersecurity #DataGovernance #EnterpriseAI #TechnologyLeadership

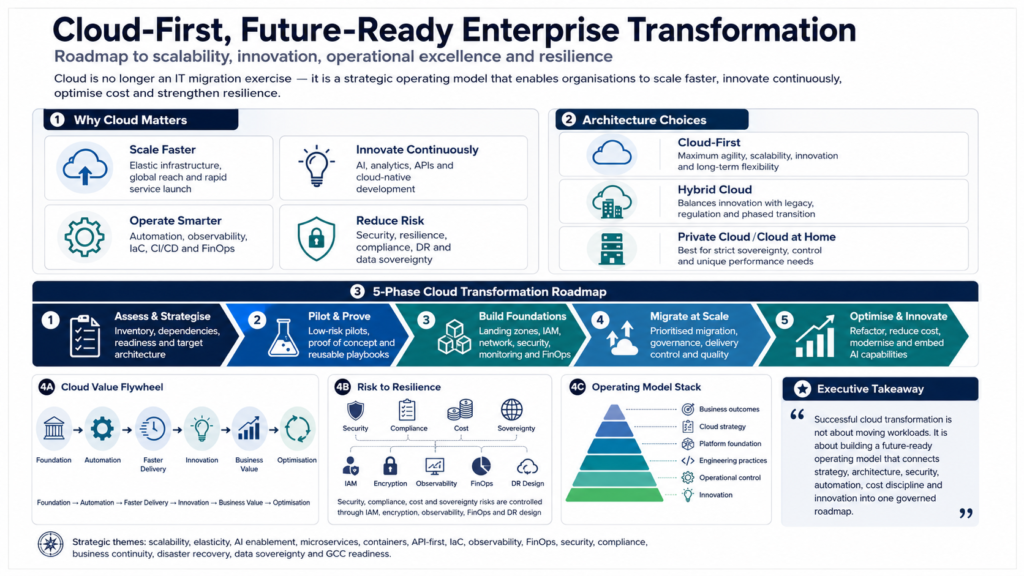

Cloud-First, Future-Ready: A Roadmap for Success

Why cloud adoption is key to scalability, innovation and operational excellence Introduction The digital landscape has fundamentally shifted. Organisations today face unprecedented pressure to innovate rapidly, scale efficiently, and remain resilient in the face of disruption. Cloud computing has emerged not merely as a technology choice, but as a strategic imperative that shapes how enterprises compete, operate, and evolve. For chief information officers (CIOs), chief technology officers (CTOs), and enterprise leaders, the question is no longer whether to adopt cloud technologies, but how to do so strategically. A cloud-first approach offers transformative potential—enabling organisations to respond to market changes faster, innovate at scale, and optimise operational costs. Yet this transformation is not a single-step migration; it requires a carefully orchestrated strategy that balances innovation with risk management, agility with governance, and transformation with stability. This article examines the strategic rationale for cloud adoption, explores multiple architectural approaches (cloud-first, hybrid, and on-premises), and provides a roadmap to achieve scalability, innovation, and operational excellence while managing inherent risks and ensuring organisational resilience. 1. The Business Case for Cloud: Strategic Imperatives Scalability and Elasticity Cloud platforms fundamentally redefine how organisations think about infrastructure. Traditional on-premises environments require capital-intensive investments in physical hardware, with capacity planning cycles that extend months into the future. Cloud architectures eliminate this constraint. Resources scale automatically based on demand, whether responding to seasonal traffic spikes, sudden user growth, or real-time workload fluctuations. For enterprises operating in the GCC region—where digital transformation initiatives frequently target rapid user acquisition, real-time transactions, and global service delivery—this elasticity translates to tangible competitive advantage. An organisation can launch new services, expand into new markets, or accommodate rapid scaling without the procurement delays and capital expenditure that constrain on-premises alternatives. Innovation Acceleration Cloud platforms democratize access to advanced technologies. Machine learning, artificial intelligence, data analytics, Internet of Things (IoT), and advanced security services—capabilities historically available only to technology leaders with substantial R&D budgets—are now accessible to organisations of any size via cloud services. This accessibility accelerates time-to-market for new capabilities. Development teams can experiment with emerging technologies, validate business hypotheses at low cost, and rapidly scale successful initiatives. Cloud-native development patterns—microservices, containerization, serverless computing—enable organisations to build modular, independently deployable applications that evolve more rapidly than monolithic architectures. The result is an organisation that innovates continuously rather than in quarterly or annual releases. Operational Excellence and Cost Optimisation Cloud infrastructure eliminates capital expenditure for hardware, facilities, and associated operational overhead. Organisations shift from paying for peak capacity (which sits idle during off-peak periods) to paying for actual consumption. This consumption-based model, when combined with cloud-native architectural patterns, substantially reduces the total cost of ownership. Beyond cost, cloud platforms provide comprehensive operational visibility. Native monitoring, logging, and analytics capabilities enable teams to understand system behaviour in detail, identify bottlenecks, and continuously optimise performance. Automated deployment pipelines, infrastructure-as-code, and policy-driven governance reduce manual operational effort and human error. In the GCC context, where labour costs are high and specialised technical talent is relatively scarce, the operational leverage provided by cloud platforms is particularly valuable. Organisations can accomplish more with smaller operational teams, freeing resources for strategic initiatives rather than routine infrastructure management. 2. Architectural Strategy: Cloud-First, Hybrid, and On-Premises Cloud adoption is not monolithic. Organisations must choose from distinct architectural approaches, each with specific advantages, constraints, and strategic implications. These decisions fundamentally shape technology roadmaps, operational models, and organisational capabilities for years to come. Cloud-First Architecture A cloud-first approach makes cloud the default platform for new applications, data, and infrastructure. Legacy systems migrate to the cloud when feasible; new capabilities are born in cloud environments. This strategy maximises the benefits outlined above: scalability, innovation velocity, and operational efficiency. Cloud-first is optimal when the organisation has the technical maturity to embrace cloud-native development practices, when regulatory constraints permit data residency in public clouds, and when the IT team has the capacity to modernise legacy systems. Technology leaders increasingly adopt this strategy because it provides the greatest long-term flexibility and competitive advantage. Hybrid Cloud Architecture Hybrid cloud environments span both cloud and on-premises infrastructure, with integrated operations, shared data, and coordinated workload deployment. This approach balances innovation with prudence, allowing organisations to move forward while maintaining investments in existing infrastructure. Hybrid architectures are strategically valuable in several contexts. Regulatory requirements may mandate data residency; hybrid allows organisations to maintain sensitive data on-premises while leveraging the cloud for non-sensitive workloads. Legacy applications with complex interdependencies may be impractical to migrate immediately; a hybrid approach allows them to coexist with cloud-native applications. Performance-sensitive workloads may benefit from proximity to on-premises infrastructure while other components operate in the cloud. However, hybrid architectures introduce operational complexity. Managing consistent security policies, data governance, and monitoring across disparate environments requires sophisticated tooling and organisational discipline. The long-term strategic trajectory should be toward either a committed cloud-first or a committed on-premises approach; sustained hybrid approaches often represent transitional states rather than stable end-states. On-Premises (Cloud at Home) Some organisations deploy cloud infrastructure technologies within their own data centres, leveraging containerization, Kubernetes, and cloud-native operational patterns without moving data beyond their physical control. This approach—sometimes called “cloud at home” or private cloud—offers cloud-like operational benefits while maintaining complete data sovereignty and control. This strategy appeals to organisations with stringent data sovereignty requirements, those operating in heavily regulated industries, or those with unique performance requirements. However, it requires significant investment in infrastructure expertise and does not provide the elasticity or cost advantages of public cloud. Organisations pursuing this path must have the technical depth to manage cloud infrastructure independently. 3. Enabling Scalability Through Cloud Architecture Scalability requires more than simply deploying to cloud infrastructure; it demands architectural decisions that enable systems to grow without proportional increases in complexity, cost, or operational overhead. Microservices and Modular Design Cloud-native architectures decompose applications into small, independently deployable services. Each service owns a specific business capability, maintains its own data, and communicates with other services through well-defined interfaces. This modularity enables teams to scale individual services independently based on specific demand

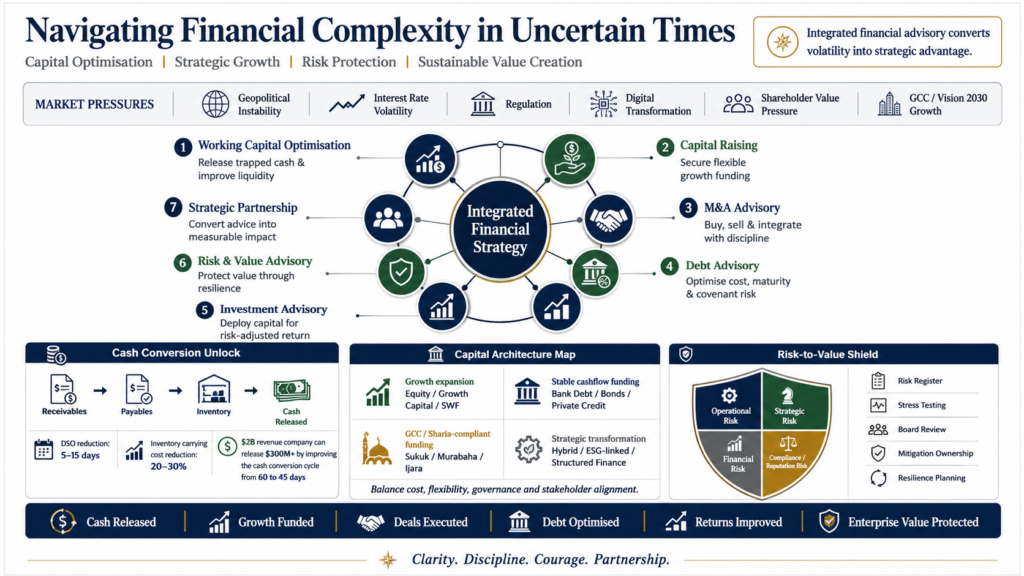

Navigating Financial Complexity in Uncertain Times

Comprehensive Strategies for Capital Optimisation, Strategic Growth, and Sustainable Value Creation Executive Overview The contemporary business landscape presents unprecedented challenges and opportunities. Organisations worldwide face a complex constellation of pressures: geopolitical instability, volatile interest-rate environments, evolving regulatory frameworks, digital transformation imperatives, and the perpetual need to deliver shareholder value amid economic uncertainty. In the Middle East and the GCC region—a market characterised by rapid transformation, diversification away from hydrocarbon dependence, and aggressive Vision 2030 objectives—these pressures are amplified by distinctive market dynamics, competitive intensity, and the imperative to balance innovation with cultural and regulatory stewardship. Success in this environment demands more than operational efficiency or tactical cost management. It requires a comprehensive, integrated approach to financial strategy that simultaneously addresses multiple imperatives: optimising working capital and cash flow, securing appropriate capital structures for growth, identifying and executing high-value M&A opportunities, managing debt strategically, identifying investment opportunities, and protecting enterprise value against emerging risks. These challenges cannot be addressed in isolation. They demand cross-functional expertise, market intelligence, and strategic foresight applied with precision and urgency. This article examines seven interconnected pillars of financial strategy and advisory excellence, providing practical frameworks and actionable guidance for senior executives, boards, and financial leaders seeking to navigate uncertainty with confidence and clarity. 1. Working Capital Optimisation: Unlocking Cash Flow in Uncertain Times Working capital—the lifeblood of operational continuity—has become the silent hero of financial performance. In uncertain macroeconomic conditions, the ability to convert operational assets into cash, reduce financing costs, and maintain liquidity provides a competitive advantage far disproportionate to its often-overlooked status in strategic discussions. The Strategic Imperative Organisations typically lock 15–25% of annual revenues in working capital—cash that could fund growth initiatives, retire debt, finance R&D, or strengthen balance-sheet resilience. In high-growth or cyclical industries, this percentage can exceed 40%. Each day of excess working capital ties up cash, increases financing costs, and constrains strategic flexibility. Conversely, aggressive working capital optimisation can free up substantial capital without requiring external financing, capex reductions, or operational compromises. Practical Optimisation Strategies Effective working capital management addresses three interconnected dimensions: The cumulative impact is substantial. A manufacturing organisation with $2B in annual revenue and a 60-day cash conversion cycle can liberate $300M+ by optimising to a 45-day cycle—capital that requires no external financing, no capex reduction, and no operational compromise. 2. Capital Raising: Securing Growth Funding with Strategic Clarity Growth requires capital. Whether funding organic expansion, entering adjacent markets, building digital capabilities, or executing transformational change, organisations must secure funding efficiently and on terms aligned with strategic objectives. Capital-raising decisions have multiyear implications for shareholder value, leverage ratios, strategic flexibility, and governance dynamics. The Capital Architecture Decision Contemporary organisations enjoy unprecedented diversity in capital sources: traditional equity and bank debt, venture capital and growth equity, private credit and structured finance, sovereign wealth and family office capital, ESG-linked financing, and hybrid instruments that blend equity and debt characteristics. The optimal capital structure reflects the organisation’s risk profile, growth trajectory, existing liabilities, shareholder base, strategic objectives, and market conditions. Equity Capital Equity capital—whether through IPO, private placement, secondary offerings, or venture/growth investment—provides capital without mandatory debt service obligations. However, equity dilutes existing shareholders and introduces new stakeholders with governance implications. IPOs unlock liquidity, provide acquisition currency, and signal market validation. However, they demand sustained profitability, quarterly disclosure obligations, and responsiveness to public market sentiment. Private equity provides growth capital, operational expertise, and network access, but typically demands strong returns and defined exit timelines. Family offices and SWFs increasingly participate in growth equity, often providing patient capital aligned with long-term value creation. Debt Capital Debt capital—bank facilities, bonds, private credit, structured finance—provides capital with defined repayment obligations and interest costs. Well-structured debt enhances returns to equity (through leverage) when the cost of debt is lower than the return on incremental capital deployed. However, excessive leverage constrains strategic flexibility, increases financial risk, and can trigger covenant breaches during downturns. The optimal debt level reflects cash flow stability, asset collateral, leverage ratios relative to peers, and access to capital markets. In the GCC context, organisations benefit from significant capital availability through sovereign wealth funds, Islamic finance instruments (such as Sukuk, Murabaha, and Ijara structures), and regional investment banks, alongside global capital markets. Strategic capital raising integrates these diverse sources into a coherent structure, optimising cost, flexibility, and stakeholder alignment. 3. M&A Advisory: Buying, Selling, and Merging with Confidence Mergers, acquisitions, and combinations represent quantum shifts in strategic position. Done well, they accelerate growth, add capabilities, enter markets, acquire talent and technology, or achieve cost synergies. Done poorly, they destroy shareholder value, distract management, and create integration chaos. The difference typically lies not in deal enthusiasm but in disciplined preparation, rigorous evaluation, and realistic integration planning. Buy-Side Advisory Acquisition strategy should begin with crystal clarity regarding the strategic rationale: market expansion, adjacent capabilities, technology or talent acquisition, competitive consolidation, cost synergies, or portfolio optimisation? Acquisitions with vague rationale frequently underperform. Due diligence must extend beyond financial statements to encompass commercial dynamics, customer concentration and retention, technology architecture and technical debt, organisational culture and talent retention, competitive positioning, regulatory exposure, and integration complexity. Valuation discipline is essential. The temptation to overpay—whether due to competitive pressure, deal fatigue, or enthusiasm for a strategic rationale—frequently destroys acquisition value. Sophisticated buy-side teams model deal returns under multiple scenarios, establish walk-away prices, and maintain patience to pass on overpriced opportunities. Sell-Side Advisory Exit decisions—whether for maturing companies, portfolio rationalisation, or founder liquidity—demand clarity regarding valuation objectives, timeline flexibility, stakeholder alignment, and operational readiness. Sell-side advisors manage the process to maximise valuation while minimising business disruption. Market preparation—financial statement enhancement, operational documentation, management readiness—typically adds 15–25% valuation premium relative to unprepared processes. Multiple buyer conversations create competitive tension that drives price realisation. Structured data rooms, synchronised due diligence, and disciplined process management protect confidentiality while enabling buyer evaluation. Merger Integration Deal completion marks the beginning, not the end. Integration—capturing synergies, retaining talent, addressing cultural differences, rationalising systems, and maintaining operational continuity—determines value realisation. Best-practice integration approaches establish: clear