Comprehensive Strategies for Capital Optimisation, Strategic Growth, and Sustainable Value Creation

Executive Overview

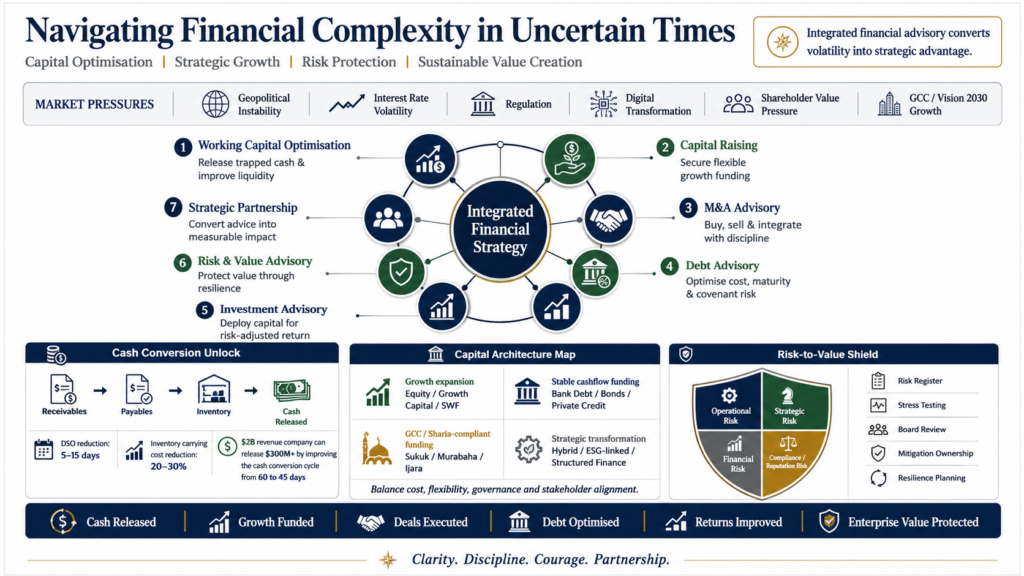

The contemporary business landscape presents unprecedented challenges and opportunities. Organisations worldwide face a complex constellation of pressures: geopolitical instability, volatile interest-rate environments, evolving regulatory frameworks, digital transformation imperatives, and the perpetual need to deliver shareholder value amid economic uncertainty. In the Middle East and the GCC region—a market characterised by rapid transformation, diversification away from hydrocarbon dependence, and aggressive Vision 2030 objectives—these pressures are amplified by distinctive market dynamics, competitive intensity, and the imperative to balance innovation with cultural and regulatory stewardship.

Success in this environment demands more than operational efficiency or tactical cost management. It requires a comprehensive, integrated approach to financial strategy that simultaneously addresses multiple imperatives: optimising working capital and cash flow, securing appropriate capital structures for growth, identifying and executing high-value M&A opportunities, managing debt strategically, identifying investment opportunities, and protecting enterprise value against emerging risks. These challenges cannot be addressed in isolation. They demand cross-functional expertise, market intelligence, and strategic foresight applied with precision and urgency.

This article examines seven interconnected pillars of financial strategy and advisory excellence, providing practical frameworks and actionable guidance for senior executives, boards, and financial leaders seeking to navigate uncertainty with confidence and clarity.

1. Working Capital Optimisation: Unlocking Cash Flow in Uncertain Times

Working capital—the lifeblood of operational continuity—has become the silent hero of financial performance. In uncertain macroeconomic conditions, the ability to convert operational assets into cash, reduce financing costs, and maintain liquidity provides a competitive advantage far disproportionate to its often-overlooked status in strategic discussions.

The Strategic Imperative

Organisations typically lock 15–25% of annual revenues in working capital—cash that could fund growth initiatives, retire debt, finance R&D, or strengthen balance-sheet resilience. In high-growth or cyclical industries, this percentage can exceed 40%. Each day of excess working capital ties up cash, increases financing costs, and constrains strategic flexibility. Conversely, aggressive working capital optimisation can free up substantial capital without requiring external financing, capex reductions, or operational compromises.

Practical Optimisation Strategies

Effective working capital management addresses three interconnected dimensions:

- Receivables Management: Optimise Days Sales Outstanding (DSO) through improved billing processes, credit policy calibration, early payment discounts, dynamic discounting platforms, and sophisticated collection management. Organisations implementing digital invoice processing and automated payment reconciliation frequently reduce DSO by 5–15 days, unlocking millions in cash.

- Payables Optimisation: Strategic extension of Days Payables Outstanding (DPO) without supplier relationship damage or reputational cost. Initiatives include supply chain financing arrangements, reverse factoring platforms, early payment discount analysis, and vendor consolidation. Supply chain financing can extend the cash runway by weeks or months while, paradoxically, improving supplier relationships through greater visibility and predictability.

- Inventory Optimisation: Reduce Days Inventory Outstanding (DIO) through demand sensing, safety stock optimisation, supply chain visibility enhancement, and category-specific inventory strategies. Seasonal and cyclical adjustments, coupled with improved demand forecasting and supplier agility, can reduce inventory carrying costs by 20–30% while maintaining service levels.

The cumulative impact is substantial. A manufacturing organisation with $2B in annual revenue and a 60-day cash conversion cycle can liberate $300M+ by optimising to a 45-day cycle—capital that requires no external financing, no capex reduction, and no operational compromise.

2. Capital Raising: Securing Growth Funding with Strategic Clarity

Growth requires capital. Whether funding organic expansion, entering adjacent markets, building digital capabilities, or executing transformational change, organisations must secure funding efficiently and on terms aligned with strategic objectives. Capital-raising decisions have multiyear implications for shareholder value, leverage ratios, strategic flexibility, and governance dynamics.

The Capital Architecture Decision

Contemporary organisations enjoy unprecedented diversity in capital sources: traditional equity and bank debt, venture capital and growth equity, private credit and structured finance, sovereign wealth and family office capital, ESG-linked financing, and hybrid instruments that blend equity and debt characteristics. The optimal capital structure reflects the organisation’s risk profile, growth trajectory, existing liabilities, shareholder base, strategic objectives, and market conditions.

Equity Capital

Equity capital—whether through IPO, private placement, secondary offerings, or venture/growth investment—provides capital without mandatory debt service obligations. However, equity dilutes existing shareholders and introduces new stakeholders with governance implications. IPOs unlock liquidity, provide acquisition currency, and signal market validation. However, they demand sustained profitability, quarterly disclosure obligations, and responsiveness to public market sentiment. Private equity provides growth capital, operational expertise, and network access, but typically demands strong returns and defined exit timelines. Family offices and SWFs increasingly participate in growth equity, often providing patient capital aligned with long-term value creation.

Debt Capital

Debt capital—bank facilities, bonds, private credit, structured finance—provides capital with defined repayment obligations and interest costs. Well-structured debt enhances returns to equity (through leverage) when the cost of debt is lower than the return on incremental capital deployed. However, excessive leverage constrains strategic flexibility, increases financial risk, and can trigger covenant breaches during downturns. The optimal debt level reflects cash flow stability, asset collateral, leverage ratios relative to peers, and access to capital markets.

In the GCC context, organisations benefit from significant capital availability through sovereign wealth funds, Islamic finance instruments (such as Sukuk, Murabaha, and Ijara structures), and regional investment banks, alongside global capital markets. Strategic capital raising integrates these diverse sources into a coherent structure, optimising cost, flexibility, and stakeholder alignment.

3. M&A Advisory: Buying, Selling, and Merging with Confidence

Mergers, acquisitions, and combinations represent quantum shifts in strategic position. Done well, they accelerate growth, add capabilities, enter markets, acquire talent and technology, or achieve cost synergies. Done poorly, they destroy shareholder value, distract management, and create integration chaos. The difference typically lies not in deal enthusiasm but in disciplined preparation, rigorous evaluation, and realistic integration planning.

Buy-Side Advisory

Acquisition strategy should begin with crystal clarity regarding the strategic rationale: market expansion, adjacent capabilities, technology or talent acquisition, competitive consolidation, cost synergies, or portfolio optimisation? Acquisitions with vague rationale frequently underperform. Due diligence must extend beyond financial statements to encompass commercial dynamics, customer concentration and retention, technology architecture and technical debt, organisational culture and talent retention, competitive positioning, regulatory exposure, and integration complexity. Valuation discipline is essential. The temptation to overpay—whether due to competitive pressure, deal fatigue, or enthusiasm for a strategic rationale—frequently destroys acquisition value. Sophisticated buy-side teams model deal returns under multiple scenarios, establish walk-away prices, and maintain patience to pass on overpriced opportunities.

Sell-Side Advisory

Exit decisions—whether for maturing companies, portfolio rationalisation, or founder liquidity—demand clarity regarding valuation objectives, timeline flexibility, stakeholder alignment, and operational readiness. Sell-side advisors manage the process to maximise valuation while minimising business disruption. Market preparation—financial statement enhancement, operational documentation, management readiness—typically adds 15–25% valuation premium relative to unprepared processes. Multiple buyer conversations create competitive tension that drives price realisation. Structured data rooms, synchronised due diligence, and disciplined process management protect confidentiality while enabling buyer evaluation.

Merger Integration

Deal completion marks the beginning, not the end. Integration—capturing synergies, retaining talent, addressing cultural differences, rationalising systems, and maintaining operational continuity—determines value realisation. Best-practice integration approaches establish: clear governance and decision rights; dedicated integration leadership with organisational authority; detailed 100-day plans addressing critical priorities; synergy identification with accountability and ownership; communication cadence to stakeholders, internal and external; and flexibility to adjust plans as new realities emerge. Organisations that prepare integration plans pre-close, engage management at every level, and maintain disciplined execution frequently realise 80–100% of modelled synergies. Those without structured integration often realise <50%.

4. Debt Advisory: Optimising Financing Structure

Debt is not a monolithic commodity. Organisations can structure debt in numerous configurations—banks vs capital markets, fixed vs floating rate, secured vs unsecured, senior vs subordinated, straight debt vs instruments with equity features—each with distinct implications for cost, flexibility, and covenant risk. Optimal debt structure reflects cash flow characteristics, balance sheet capacity, market access, and strategic objectives.

Debt Refinancing and Restructuring

In volatile rate environments, refinancing opportunities emerge regularly. Organisations with maturing debt should continuously evaluate refinancing windows—whether to lock favourable rates, extend maturities, or modify covenant structures. Sophisticated treasury functions maintain detailed maturity ladders, monitor the rate environment, and execute refinancings when the economics align. Equally important: refinancing distressed debt structures before covenant pressures force reactive negotiations. Proactive restructuring—before breaches occur—typically achieves more favourable terms and preserves stakeholder relationships.

Islamic Finance and Sukuk

In the GCC context, Islamic finance instruments provide distinctive advantages. Sukuk (Islamic bonds), Murabaha facilities (cost-plus financing), Ijara (leasing), and Musharaka (profit-sharing) structures offer both religious compliance and often competitive pricing. Sukuk issuances across the GCC provide access to deep investor bases and potentially lower funding costs. Organisations operating across Islamic and conventional markets benefit from capabilities in both, enabling capital structure optimisation that balances stakeholder preferences and market opportunities.

5. Investment Advisory: Identifying and Maximising Returns

Beyond operational capital deployment, organisations accumulate capital—through cash generation, insurance proceeds, pension fund performance, or strategic divestitures—that must be deployed with discipline. Investment returns compound over years and decades. A 200 basis point difference in return on $100M of capital generates $2M annual incremental value in perpetuity—equivalent to $20–30M of enterprise value at typical multiples.

Investment Strategy

Investment strategy should reflect organisational mandate, risk tolerance, liquidity requirements, and return objectives. Family offices and sovereign wealth funds increasingly employ sophisticated multi-asset strategies—combining public equities, private markets (PE, VC), real assets (infrastructure, real estate), fixed income, and alternative investments. Traditional corporations often maintain more conservative approaches: high-grade fixed income, liquidity funds, and defensive equity. Investment decisions should increasingly incorporate ESG considerations that are material to long-term value, risk management, and stakeholder expectations. In the GCC context, significant capital increasingly flows to Vision 2030 priority sectors—renewable energy, diversified manufacturing, fintech, healthcare, tourism—where returns and societal impact align.

Portfolio Construction

Effective investment advisors construct portfolios reflecting diversification principles, correlation analysis, risk budgeting, and return optimisation. They stress-test portfolios against adverse scenarios, establish rebalancing protocols, manage tax efficiency, and adapt to changing market conditions. The difference between competent and exceptional investment management often appears modest on annual statements but compounds to substantial value over decades. For large institutional portfolios ($500M+), the difference between 5% and 7% annual returns equals hundreds of millions in incremental value over investment horizons.

6. Risk and Value Advisory: Building Resilience

Enterprise value emerges from three interconnected sources: operational excellence (generating returns above the cost of capital), strategic positioning (competitive advantage and market dynamics), and financial engineering (optimal capital structure and tax efficiency). Risk advisory protects value by identifying threats before they crystallise into crises, and designing mitigation strategies with discipline and clarity.

Risk Identification and Governance

Comprehensive risk frameworks encompass operational risks (process failures, talent loss, customer concentration), strategic risks (market disruption, competitive displacement, regulatory change), financial risks (credit, liquidity, interest rate, foreign exchange), and reputational/compliance risks (governance failures, regulatory violations, reputation damage). Sophisticated organisations maintain risk registers with clear ownership, mitigation strategies, escalation protocols, and monitoring cadence. Board-level risk committees review critical risks quarterly, stress-test scenarios, and challenge management mitigation assumptions.

Resilience Planning

Resilience extends beyond crisis management to encompass sustainability under adverse conditions. Organisations build resilience through: supply chain diversification and visibility, operational flexibility that enables rapid adaptation, financial buffer capacity (cash reserves, undrawn credit facilities), stakeholder relationship strength, and organisational culture that emphasises accountability and transparency. Stress testing—modelling performance under severe scenarios (30% revenue decline, 40% cost inflation, loss of a key customer, regulatory sanction)—reveals vulnerabilities that require mitigation. Organisations that have stress-tested scenarios navigate actual disruptions far more effectively than those managing by surprise.

7. Strategic Partnership: Trusted Advisors for Lasting Impact

The distinguishing characteristic of exceptional advisory partnerships is not technical expertise—commoditised across capable firms—but rather strategic alignment, executive engagement, organisational impact, and measurable value creation. Trusted advisors operate at multiple organisational levels simultaneously: board engagement, providing a governance perspective; CFO partnership on strategic initiatives; operational integration with functional teams; and ownership accessibility for major decisions.

Effective partnerships feature: deep understanding of industry dynamics and competitive positioning; access to distinctive market intelligence and transactions; financial modelling sophistication and creativity; organisational change management capability; and a track record of successful outcomes. Trusted advisors not only identify problems but also structure solutions, navigate organisational dynamics, and ensure sustainable implementation.

Navigating Forward: Integrated Financial Strategy

The seven pillars outlined—working capital optimisation, capital raising, M&A advisory, debt advisory, investment advisory, risk and value protection, and strategic partnership—are not independent domains but interconnected elements of a comprehensive financial strategy. An organisation pursuing aggressive growth through acquisition requires an appropriate capital structure, robust risk management, working-capital discipline to fund growth, and strategic clarity on returns. A mature organisation harvesting cash must optimise every dollar through working capital efficiency, invest excess capital strategically, manage refinancing risk, and maintain resilience against disruption.

In the distinctive context of the GCC—experiencing rapid transformation, Vision 2030 diversification initiatives, technological disruption, and demographic dynamism—organisations face both distinctive opportunities and complex challenges. Those that integrate financial strategy across all dimensions, execute with discipline, and partner with advisors who combine expertise with intimate market understanding emerge as winners. Those managing financial dimensions in silos, operating reactively, or relying on generic advice face headwinds.

The path forward demands clarity of strategic intent, discipline in execution, courage to make difficult decisions, and partnership with advisors who understand both the technical dimensions of finance and the organisational dynamics of sustainable value creation. In uncertain times, those characteristics—clarity, discipline, courage, and partnership—distinguish the organisations that not only survive but thrive.

For organisations seeking to navigate financial complexity with strategic confidence, the conversation begins with clarity on objectives, an honest assessment of current capabilities and constraints, and the collaborative design of initiatives that address the most material opportunities and risks.