The Silent Risk: What Happens When Nothing Changes

The Comfort of Success: A Dangerous Assumption There is a particular comfort that comes with running a successful business for decades. Markets have been kind. The founder has built something substantial. Cash flows are healthy. The customer base is loyal. Employees have been with the company for years. Suppliers know how to work with the business. The regulatory environment is stable. The business has succeeded by doing what it has always done. This success creates a particularly dangerous psychological dynamic: the assumption that continued success requires nothing more than maintaining current approaches. This assumption is understandable. It is also potentially catastrophic. Because the external environment in which family businesses operate is not static. Markets are changing. Competition is intensifying. Technology is disrupting traditional business models. Customer preferences are evolving. Regulatory frameworks are becoming more stringent. The labour market is shifting. Generational expectations are changing. Stability and unchanging operations, which were the source of past success, become the source of future decline. The Risk Landscape: What Changes and What It Means To understand the silent risk of inaction, we must examine the external environment changes that are transforming business conditions across the GCC: Market Consolidation and New Competition For decades, many family businesses operated in industries with a stable, predictable competitive landscape. The top three players remained the top three players. New competitors entered rarely and with difficulty. Margins were sustainable. This is changing. Several forces are driving market disruption: Global multinationals are increasingly comfortable operating in GCC markets. Walmart entered through Carrefour’s ownership. Amazon is building regional logistics capabilities. FMCG multinationals are improving distribution directly, reducing dependence on traditional distributors. Professional management is becoming table stakes, not a competitive advantage. Technology-enabled competitors are emerging. E-commerce platforms are consolidating retail, eating into traditional retail margins. Digital marketplaces are disintermediating traditional distribution models. FinTech platforms are competing with traditional financial services. Regional players from adjacent markets are expanding across borders. An excellent distributor from Egypt or Saudi Arabia sees an opportunity in the UAE market and enters with modern approaches and lower cost structures. Within the GCC, family businesses are consolidating, creating super-competitors with greater scale, specialised functions, and operational sophistication. The consequence: The stable competitive environment that has characterised many industries is becoming unstable. A secure market position is becoming vulnerable. A company that was the clear category leader is facing new competitors and margin pressure. A family business that assumes it will maintain its market position through existing approaches is operating from a dangerous assumption. Changing Customer Expectations Customer expectations are evolving in ways that many traditional family businesses have not fully internalised. Digital-native customers (typically younger, educated abroad, exposed to global consumer experiences) have different expectations: Traditional family businesses that excel at personal relationships and in-person service often lag in digital capabilities and omnichannel experience. A retail business that was world-class in in-store experience may be fundamentally unprepared for e-commerce competition. Similarly, B2B customer expectations are evolving. Large corporate customers increasingly demand integration with digital platforms, real-time visibility into supply chains, and data-driven reporting. A distribution company that sold through personal relationships and phone orders is competing with suppliers that offer cloud-based ordering platforms and automated fulfilment. Customers are not loyal forever, and not to traditional approaches. Loyalty is to companies that meet evolving expectations. A business that ignores these changes loses market share to more responsive competitors. Technological Disruption The pace of technology change is accelerating. Technologies that were science fiction a decade ago are now accessible and affordable: A family business that does not embrace technology will find itself unable to compete with companies that do. A manufacturing company without ERP visibility into production costs will lose margin competition to one with real-time production analytics. A retail company without e-commerce will lose market share to those with seamless digital experiences. Technology is not a nice-to-have. It is becoming table stakes. Regulatory and Compliance Evolution The GCC regulatory environment is tightening. Governments are moving toward formalisation, transparency, and standardisation in ways that were not previously required. Examples: A family business that assumes regulatory requirements will remain static is making a dangerous assumption. Compliance is evolving, and non-compliance has increasing costs. Talent Market Changes The labour market is fundamentally shifting, and this has particular implications for family businesses: Younger employees expect: Traditional family businesses that have retained employees through personal relationships, informal advancement, and family proximity are finding that this model no longer works. Superior talent is increasingly choosing to work for professional organisations with clear career paths, competitive compensation, and recognised brands over family businesses with opaque advancement and informal processes. The consequence: Family businesses are losing their best employees to more professional competitors. The institutional knowledge that was retained through employee loyalty is walking out the door. Additionally, the cost of replacement talent has increased substantially. Recruiting, training, and retaining new talent requires investment in systems, processes, and compensation that traditional family businesses may not have budgeted for. Demographic and Generational Shifts UAE demographics are changing in ways that affect family business sustainability: The founder generation that built family businesses is ageing. Many founders are approaching retirement or have already entered their 70s or 80s. The transition to the next generation is not a future event—it is a present event. The next generation has different worldviews and expectations. Many have been educated internationally and worked at multinational corporations or in startup environments. They expect professional management, clear governance, transparent decision-making, and strategic clarity. They do not want to inherit a business structured entirely around the founder’s discretion. Additionally, demographic composition in the GCC is changing. The Emirati population is growing at different rates than expatriate populations. Government policies are increasingly favouring Emiratization (employment of citizens). A family business that relies entirely on expatriate management may find regulatory expectations shifting toward citizen employment, forcing staffing changes. Capital Market Evolution The sources and costs of capital are evolving in ways that create pressure on family businesses: Traditional bank financing was the primary source of growth capital for family

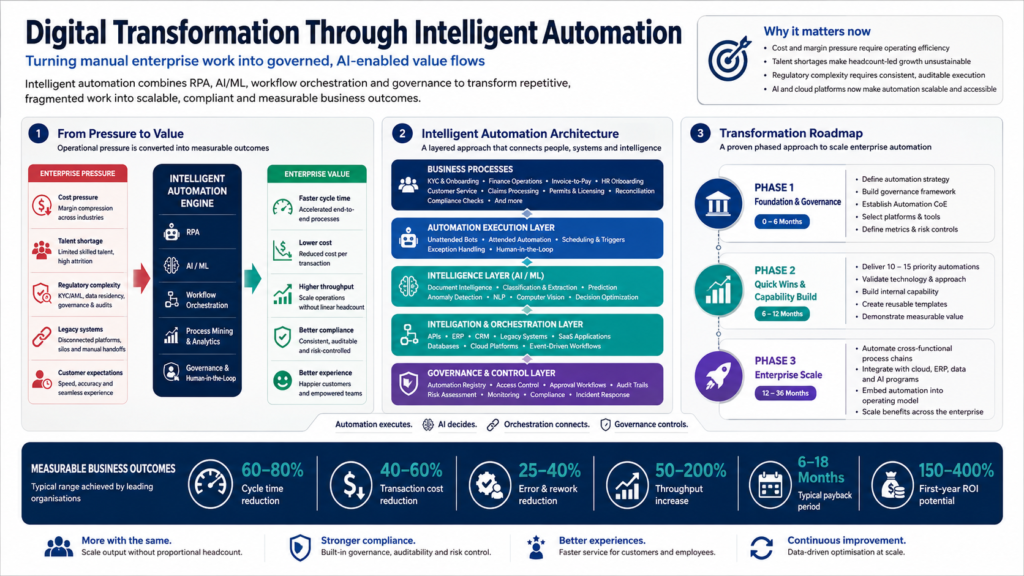

Digital Transformation Through Intelligent Automation

Driving Efficiency and Business Agility in the Modern Enterprise — Executive Summary The enterprise landscape is undergoing a fundamental shift. Digital transformation is no longer a technology initiative—it is a business imperative. At the heart of this transformation lies intelligent automation: the convergence of robotic process automation (RPA), artificial intelligence, machine learning, and workflow orchestration technologies that reimagine how organisations operate. Unlike traditional automation, which follows rigid rules and scripts, intelligent automation adapts, learns, and scales. It transforms not just how work gets done, but why and when work gets done. For organisations across the GCC and beyond, intelligent automation unlocks unprecedented efficiency, enables rapid business model evolution, and creates the agility required to compete in a digital-first economy. This article explores how leading organisations are leveraging intelligent automation to drive measurable business outcomes, the strategic imperatives underpinning successful transformation, and the governance frameworks required to scale automation across the enterprise. — Part 1: The Case for Intelligent Automation Why Now? The last five years have accelerated digital transformation timelines by a decade. The convergence of three forces has created an inflexion point: 1. Economic Pressure and Operational Resilience Organisations face unprecedented cost pressure. Talent shortages persist across the GCC region—particularly in highly technical roles—making workforce expansion unsustainable. Margin compression in traditional business models demands operational excellence. Simultaneously, regulatory complexity has increased: KYC/AML requirements, data localisation mandates, and governance frameworks now require organisations to do more with finite resources. Intelligent automation addresses this directly. It handles repetitive, rules-based work at scale without adding headcount. A financial services organisation can process KYC documents in minutes rather than days. A healthcare provider can automate insurance verification. A government entity can accelerate permit processing. The efficiency gains are often a 40-70% reduction in cycle time and a 30-50% cost reduction per transaction. 2. Technology Maturity and Accessibility Five years ago, intelligent automation was the domain of global technology leaders and well-funded enterprises. Today, cloud-native automation platforms, pre-built process templates, and low-code/no-code development tools have democratised access. Organisations no longer need to build automation from first principles. They can configure, integrate, and deploy. This democratisation has particular significance in the GCC, where many organisations have been pursuing digital transformation but lack the deep technical talent pools found in mature tech markets. Modern automation platforms now allow business analysts to design and deploy automation without requiring specialist developers. This dramatically accelerates time-to-value and lowers the barrier to entry. 3. AI/ML Readiness and Data Availability The third force is the maturation of AI and machine learning capabilities. Early automation initiatives were rules-based: IF this condition, THEN that action. Modern intelligent automation combines classical RPA with machine learning models that can classify documents, extract data, predict outcomes, and optimise routing decisions. More importantly, organisations now have the data and cloud infrastructure to train these models. Historical transaction data, process logs, and outcome metrics provide the foundation for ML models that improve with use. Cloud platforms provide the computational resources to run inference at scale without significant capital investment. For organisations across the GCC with substantial historical business data—financial transactions, customer interactions, operational records—this represents a significant untapped asset. That data can be weaponised to drive automation that is not just efficient, but intelligent and adaptive. The Business Case: Real-World Outcomes The business case for intelligent automation is compelling and well-documented across industries: Financial Services: A regional bank implemented intelligent automation across its mortgage origination process, reducing processing time from 21 days to 3 days. The automation handles document verification, data validation, compliance checking, and funding coordination. Staff were redeployed to customer-facing roles and complex exception handling. The bank processed 40% higher volume with 25% fewer FTE. Healthcare and Life Sciences: A multinational pharmaceutical company automated its invoice-to-pay process across 47 global entities. The automation handles invoice receipt, three-way matching with PO and goods receipt, exception flagging, and payment processing. This single automation reduced days payable outstanding by 8 days while improving supplier satisfaction and payment accuracy. Government and Public Sector: A GCC government entity implemented intelligent document processing for permit applications. The automation extracts information from unstructured application documents, validates it against multiple databases, cross-checks compliance requirements, and routes it to the appropriate approvers. Processing time reduced from 45 days to 5 days. Citizen satisfaction scores improved 30%. Staff handling capacity increased without adding budget. Retail and E-Commerce: A large regional retailer automated inventory reconciliation, demand forecasting, and replenishment ordering. The automation integrates POS systems, warehouse management, supplier systems, and market data. It automatically identifies discrepancies, applies predictive models to forecast demand, and generates optimised purchase orders. Stockout incidents reduced 35%. Inventory carrying costs reduced 18%. These are not theoretical outcomes. They represent measurable impact across diverse sectors and geographies. The patterns are consistent: — Part 2: Understanding Intelligent Automation Architecture The Technology Stack Intelligent automation is not a single technology but an orchestrated ecosystem. Understanding the components is essential for effective strategy and implementation. Robotic Process Automation (RPA) – The Foundation RPA is the foundational technology. RPA bots are software programs that mimic human interaction with computer systems—logging in, navigating interfaces, entering data, validating information, and copying files. Unlike middleware or API-based integration, RPA is non-invasive: it works with systems as they exist, without requiring integration development or modifications to legacy systems. This is particularly valuable in the GCC context, where many organisations operate complex landscapes of legacy systems—some built decades ago, some highly customised, some with limited vendor support. Organisations often lack the technical knowledge, budget, or vendor cooperation required to modify these systems. RPA allows organisations to automate processes across these fragmented landscapes without system-level changes. RPA is best applied to high-volume, rules-based, repetitive work: data entry, validation, copying between systems, calculation of standard formulas, and exception identification. It excels when rules are well-defined and processes are stable. Artificial Intelligence and Machine Learning – The Intelligence Layer RPA + AI = Intelligent Automation. While RPA handles execution, AI/ML adds the intelligence layer. Machine learning excels at classification (which category does this document belong

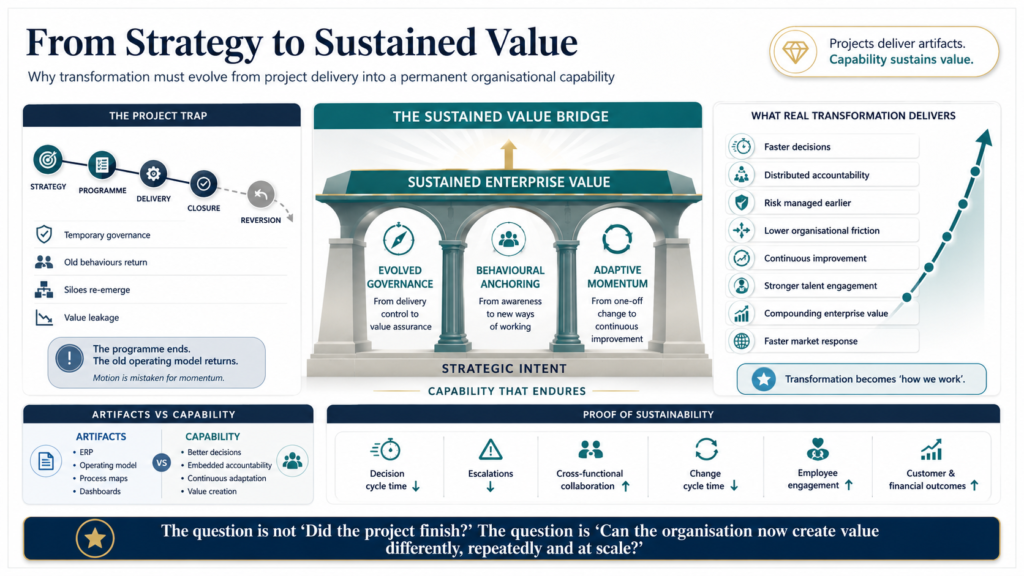

From Strategy to Sustained Value: The Transformation Imperative

Why successful transformation is about more than projects — it’s about creating lasting impact. — Most transformation initiatives fail not because the strategy is wrong, but because organisations mistake motion for momentum. They launch projects, celebrate milestones, declare victory—and then watch the organisation drift back to its original state within months. The gap between strategic intent and sustained value is where countless billions are lost each year, and understanding it is essential for any organisation seeking competitive advantage in rapidly changing markets. This gap exists because transformation is treated as a finite undertaking rather than a fundamental shift in how an organisation thinks, decides, and executes. It’s the difference between a project that ends and a capability that endures. And the distinction matters profoundly—not just for internal morale but for survival in markets where the speed of adaptation has become the primary competitive differentiator. — The Project Trap: Why Most Transformations Fade Consider the typical transformation playbook that organisations have been following for decades: You define strategic objectives, assemble a program office, organise work into deliverable workstreams, execute against a timeline, celebrate milestones, and then declare victory and close the program. By traditional project management measures, the initiative is deemed “successful.” The CIO moves on to the next initiative. Governance is stood down. External consultants and program advisors exit the organisation. The PMO either shrinks dramatically or disappears entirely. What happens in the months and years that follow tells a different story. Without active governance and systematic reinforcement, organisations fail to sustain the transformation. They revert—not overnight, but gradually, almost imperceptibly. The new operating model encounters friction from old habits and informal power structures, and people begin to work around it rather than within it. Teams slip back into familiar patterns because those patterns are easier, socially accepted, and don’t require the cognitive overhead of new ways of working. Systems that were supposed to be integrated into a seamless environment develop silos again as business units prioritise local optimisation over enterprise-wide benefit. The cultural shifts that were supposed to be permanent become footnotes in the annual review, referenced occasionally but no longer active in how people behave. The projects delivered tangible outputs—a new ERP system, a restructured organisational chart, a documented process architecture, training programs, and technology infrastructure. These are real. They exist. But the transformation itself—the sustained shift in capability, behaviour, and value creation—never took hold. This happens because the organisation never moved from doing transformation projects to being transformed. The Economics of Reversion The costs of this reversion are staggering and often hidden. A financial services organisation invests $200 million in a digital transformation program, delivers all planned systems and processes, declares success, and then watches as decision-making cycles remain as slow as before because the new system was layered onto old governance structures. An industrial company restructures for agility, only to watch the new matrix organisation calcify into the same political battlegrounds that existed before. A government agency modernises its technology platform but never reshapes how it actually makes decisions, resulting in faster access to the same suboptimal processes. In each case, the organisation spent enormous capital and consumed years of leadership attention to deliver an infrastructure for transformation that was never actually used for that purpose. The infrastructure became a new layer on top of the old operating model, creating cost without benefit. The economic loss extends beyond the direct cost of the program. There are opportunity costs—the strategic initiatives that couldn’t be undertaken because the transformation project itself consumed all available energy. There’s the erosion of organisational capability as talented people, frustrated by the gap between the promised transformation and the operating model in practice, leave for organisations where change actually happens. And there’s the strategic vulnerability that comes from spending three years and hundreds of millions in resources to end up in a position only marginally different from the starting point. Why Reversion Is Structural, Not Personal It’s tempting to blame reversion on failed change management or a lack of leadership commitment. These factors matter, but they’re not the root cause. The root cause is structural: organisations don’t maintain what they don’t measure, and they don’t measure what they don’t expect to persist. When a transformation program has an end date, everything in the program is designed around that endpoint: governance is temporary, investment is time-bound, success metrics are designed to prove the program delivered, and attention spans are calibrated to the program timeline. The organisational infrastructure—the systems that sustain behaviour change, distribute decision rights, and reinforce new practices—is never built because it isn’t within the scope of a time-bound project. The moment the program closes, the organisation returns to its default state: the operating model that evolved to handle the work the organisation actually does, which now includes whatever new systems were put in place, but not the behavioural or governance infrastructure to use them differently. — The Distinction That Matters: Artefacts Versus Capability Here’s the critical insight that separates organisations that sustain the value of transformation from those that don’t: Transformation projects deliver artefacts. Transformation capability creates value. Artefacts are important—they’re the mechanism, the foundation, the enabling infrastructure. But they are not the destination. Understanding this distinction is essential. A new enterprise resource planning system is not a transformation; it’s an enabler of transformation. The transformation occurs when information flows through the organisation without institutional friction, enabling faster, better decisions. A process map is not a transformation; it’s a blueprint. The transformation is when people actually execute work according to the new process because the incentives, capabilities, and governance structures make it the easiest path. A restructured organisation is not a transformation; it’s a structure awaiting new behaviours. The transformation is when accountability shifts, information flows differently, and people collaborate across boundaries because the structure makes it natural rather than forced. Most organisations can deliver artefacts. The evidence is everywhere: thousands of successful system implementations, process redesigns, restructurings, and technology deployments. What organisations struggle with is translating artefacts into sustained capability