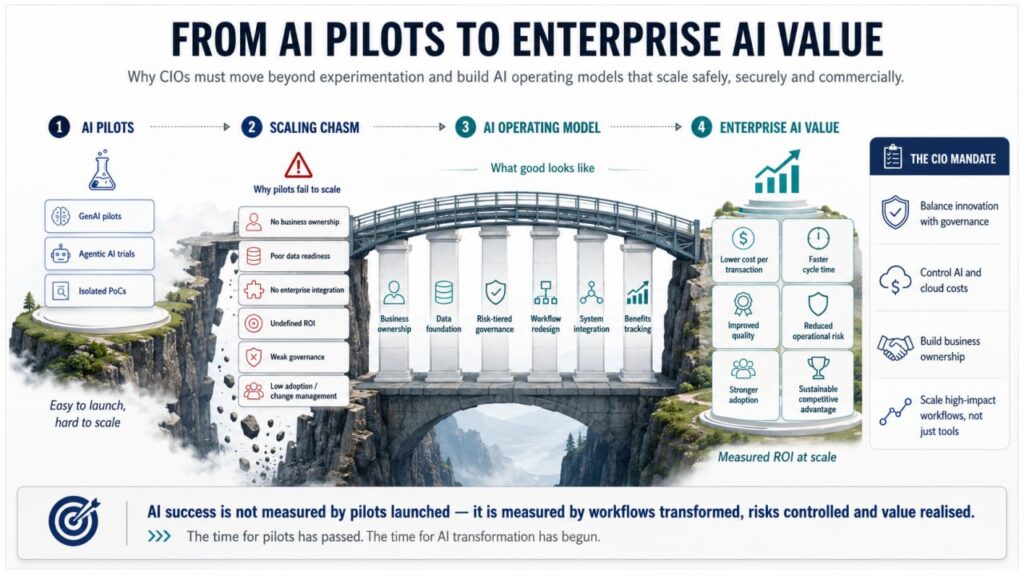

From AI Pilots to AI Value: Why CIOs Must Move Beyond Experimentation

Opening: The Pilot Paradox AI pilots are easy. AI value is hard. This statement has become the unspoken truth in enterprise technology over the past eighteen months. Walk into any boardroom across the Middle East, Asia-Pacific, or North America, and you’ll find the same story: an organisation has deployed generative AI and agentic AI initiatives, launched multiple proof-of-concept projects, perhaps even hired dedicated AI teams. Yet when the CFO asks where the measurable business value is, the room goes quiet. The statistics tell a sobering story. Recent CIO research highlights that operationalising AI, establishing robust AI governance, ensuring data readiness, maintaining cybersecurity posture, and controlling costs are now board-level priorities. Cybersecurity remains the top CIO concern, followed closely by operationalising AI and data strategy. The challenge is no longer whether enterprises should adopt AI—that question was answered two years ago. The challenge is how to make AI work. This is not a technology problem. It is an operating model problem. Why AI Pilots Fail to Scale: The Root Causes Most enterprises fail to realise enterprise-wide value from AI pilots for a remarkably consistent set of reasons. Understanding these failure patterns is the first step toward building sustainable AI at scale. The Lack of Business Ownership The first and most critical failure point is the absence of genuine business ownership. Too many AI initiatives are launched by the technology function, often with enthusiasm from Chief Technology Officers or innovation teams, but without a clear business sponsor who owns the outcomes. When pilot projects deliver promising results in controlled environments, there is no senior business leader with the budget, authority, and accountability to champion the transition to production. This creates a dangerous dynamic. The technology team can demonstrate that the AI system works. Still, without business ownership, there is no one to advocate for the resources, process changes, governance approvals, and change management required to scale. The AI innovation becomes a laboratory curiosity rather than a business transformation initiative. Pilot success does not automatically translate to production deployment because the incentives, authorities, and governance structures are fundamentally misaligned. Inadequate Data Preparation and Governance A second critical failure is underestimating the complexity of data preparation. Generative AI and agentic AI systems require clean, well-structured, governed data. Most enterprises discover during the pilot phase that their data landscape is fragmented across legacy systems, inconsistently defined, poorly documented, and sometimes duplicated or stale. The pilot can work around these limitations. A small team can manually curate datasets, suppress noise, and work in a controlled environment. But scaling to enterprise-wide deployment requires fundamental data quality management, master data governance, data lineage, and compliance frameworks. This work is unglamorous, lengthy, and expensive. Many organisations abandon scaling plans when they confront the true scope of data work required. Moreover, without clear data governance established from the outset, pilot deployments often violate regulatory requirements, create audit risks, and leave organisations exposed to data privacy and security incidents. By the time governance frameworks are built, the damage to organisational appetite for AI expansion is already done. No Clear Integration into Enterprise Systems A third failure pattern is the isolation of AI systems from core enterprise architecture. Pilots often run on standalone platforms, fed by manually extracted data, with outputs delivered via email, dashboards, or APIs that are not integrated into the systems of record. When scaling, organisations must integrate AI systems into enterprise workflows—including ERP platforms, HCM systems, customer data platforms, and financial systems. This integration work is complex, requires changes to core business processes, and demands coordination between technology teams and business stakeholders. Many pilots never transition to this phase because the effort is underestimated or the business case for integration is unclear. Undefined Measurable ROI and Value Streams Perhaps the most damaging failure is the absence of clear, measurable ROI metrics established at the outset. Many pilots are launched with aspirational language—”improve efficiency,” “enhance decision-making,” “better customer experience”—without defining what these mean in financial or operational terms. When the time comes to scale, the business cannot articulate whether the pilot actually delivered value, whether that value is sustainable, or whether the cost of production deployment is justified. This creates a credibility gap. Executive leaders have become sceptical of AI promises; they want proof, not pilots. Missing Governance and Risk Frameworks A final critical gap is the absence of governance structures designed specifically for AI systems. Traditional IT governance does not adequately address the unique risks of AI systems: model drift, data bias, regulatory compliance, explainability requirements, liability for errors, and unintended downstream consequences. Pilots often operate in a governance vacuum. Once enterprises recognise that they need AI governance—frameworks for model monitoring, retraining, access controls, audit trails, human oversight, and regulatory compliance—many realise the scope of governance work required and pull back from scaling plans. The result is that organisations that should be at scale remain in the pilot phase, unable to move forward. The CIO’s New Challenge: Balancing Innovation with Governance The role of the Chief Information Officer has fundamentally changed. Historically, CIOs managed stability, security, and efficiency. Today’s CIOs must balance innovation velocity with risk management, security with enabling business agility, cost control with investment in capabilities that competitors are also pursuing. This balancing act is extraordinarily challenging, particularly in regulated industries like financial services and government. The pressure to innovate and adopt AI is intense—customers expect modern systems, competitors are moving fast, and board members are asking about AI strategy. Yet the risk of deploying immature AI systems into critical business processes is equally intense. The Innovation-Governance Tension The tension between innovation and governance is real and not easily resolved. Pure governance approaches kill innovation by requiring exhaustive approvals, documentation, and compliance frameworks before any AI experiment can proceed. Pure innovation approaches risk regulatory violations, operational failures, security breaches, and reputation damage. The solution is not to choose one over the other, but to design AI operating models that enable experimentation within a framework of managed risk. This requires several key elements: Sandbox environments where

The Silent Risk: What Happens When Nothing Changes

The Comfort of Success: A Dangerous Assumption There is a particular comfort that comes with running a successful business for decades. Markets have been kind. The founder has built something substantial. Cash flows are healthy. The customer base is loyal. Employees have been with the company for years. Suppliers know how to work with the business. The regulatory environment is stable. The business has succeeded by doing what it has always done. This success creates a particularly dangerous psychological dynamic: the assumption that continued success requires nothing more than maintaining current approaches. This assumption is understandable. It is also potentially catastrophic. Because the external environment in which family businesses operate is not static. Markets are changing. Competition is intensifying. Technology is disrupting traditional business models. Customer preferences are evolving. Regulatory frameworks are becoming more stringent. The labour market is shifting. Generational expectations are changing. Stability and unchanging operations, which were the source of past success, become the source of future decline. The Risk Landscape: What Changes and What It Means To understand the silent risk of inaction, we must examine the external environment changes that are transforming business conditions across the GCC: Market Consolidation and New Competition For decades, many family businesses operated in industries with a stable, predictable competitive landscape. The top three players remained the top three players. New competitors entered rarely and with difficulty. Margins were sustainable. This is changing. Several forces are driving market disruption: Global multinationals are increasingly comfortable operating in GCC markets. Walmart entered through Carrefour’s ownership. Amazon is building regional logistics capabilities. FMCG multinationals are improving distribution directly, reducing dependence on traditional distributors. Professional management is becoming table stakes, not a competitive advantage. Technology-enabled competitors are emerging. E-commerce platforms are consolidating retail, eating into traditional retail margins. Digital marketplaces are disintermediating traditional distribution models. FinTech platforms are competing with traditional financial services. Regional players from adjacent markets are expanding across borders. An excellent distributor from Egypt or Saudi Arabia sees an opportunity in the UAE market and enters with modern approaches and lower cost structures. Within the GCC, family businesses are consolidating, creating super-competitors with greater scale, specialised functions, and operational sophistication. The consequence: The stable competitive environment that has characterised many industries is becoming unstable. A secure market position is becoming vulnerable. A company that was the clear category leader is facing new competitors and margin pressure. A family business that assumes it will maintain its market position through existing approaches is operating from a dangerous assumption. Changing Customer Expectations Customer expectations are evolving in ways that many traditional family businesses have not fully internalised. Digital-native customers (typically younger, educated abroad, exposed to global consumer experiences) have different expectations: Traditional family businesses that excel at personal relationships and in-person service often lag in digital capabilities and omnichannel experience. A retail business that was world-class in in-store experience may be fundamentally unprepared for e-commerce competition. Similarly, B2B customer expectations are evolving. Large corporate customers increasingly demand integration with digital platforms, real-time visibility into supply chains, and data-driven reporting. A distribution company that sold through personal relationships and phone orders is competing with suppliers that offer cloud-based ordering platforms and automated fulfilment. Customers are not loyal forever, and not to traditional approaches. Loyalty is to companies that meet evolving expectations. A business that ignores these changes loses market share to more responsive competitors. Technological Disruption The pace of technology change is accelerating. Technologies that were science fiction a decade ago are now accessible and affordable: A family business that does not embrace technology will find itself unable to compete with companies that do. A manufacturing company without ERP visibility into production costs will lose margin competition to one with real-time production analytics. A retail company without e-commerce will lose market share to those with seamless digital experiences. Technology is not a nice-to-have. It is becoming table stakes. Regulatory and Compliance Evolution The GCC regulatory environment is tightening. Governments are moving toward formalisation, transparency, and standardisation in ways that were not previously required. Examples: A family business that assumes regulatory requirements will remain static is making a dangerous assumption. Compliance is evolving, and non-compliance has increasing costs. Talent Market Changes The labour market is fundamentally shifting, and this has particular implications for family businesses: Younger employees expect: Traditional family businesses that have retained employees through personal relationships, informal advancement, and family proximity are finding that this model no longer works. Superior talent is increasingly choosing to work for professional organisations with clear career paths, competitive compensation, and recognised brands over family businesses with opaque advancement and informal processes. The consequence: Family businesses are losing their best employees to more professional competitors. The institutional knowledge that was retained through employee loyalty is walking out the door. Additionally, the cost of replacement talent has increased substantially. Recruiting, training, and retaining new talent requires investment in systems, processes, and compensation that traditional family businesses may not have budgeted for. Demographic and Generational Shifts UAE demographics are changing in ways that affect family business sustainability: The founder generation that built family businesses is ageing. Many founders are approaching retirement or have already entered their 70s or 80s. The transition to the next generation is not a future event—it is a present event. The next generation has different worldviews and expectations. Many have been educated internationally and worked at multinational corporations or in startup environments. They expect professional management, clear governance, transparent decision-making, and strategic clarity. They do not want to inherit a business structured entirely around the founder’s discretion. Additionally, demographic composition in the GCC is changing. The Emirati population is growing at different rates than expatriate populations. Government policies are increasingly favouring Emiratization (employment of citizens). A family business that relies entirely on expatriate management may find regulatory expectations shifting toward citizen employment, forcing staffing changes. Capital Market Evolution The sources and costs of capital are evolving in ways that create pressure on family businesses: Traditional bank financing was the primary source of growth capital for family

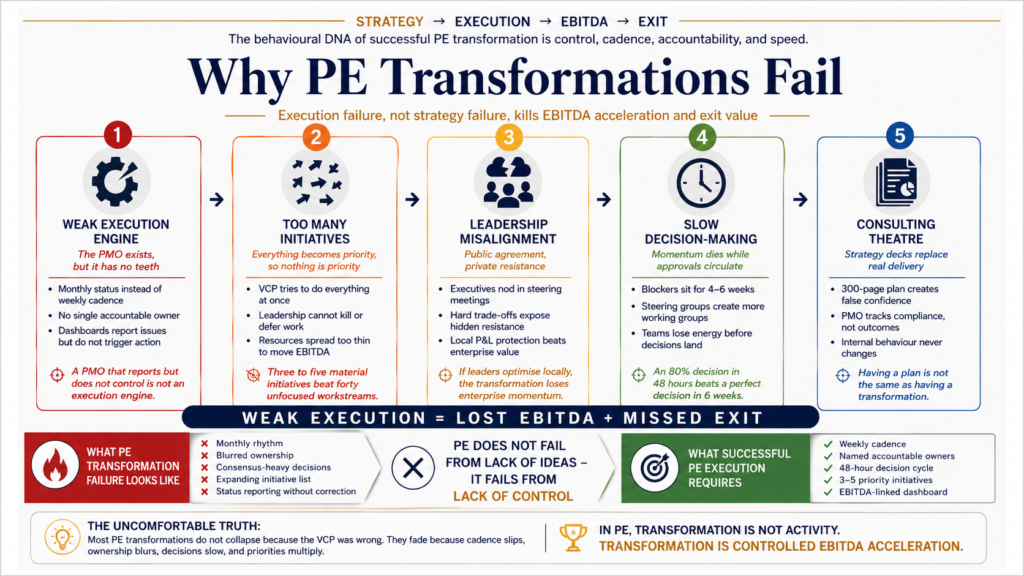

Why Most PE Transformations Fail (And No One Talks About It)

The Uncomfortable Truth About Execution, Not Strategy Private Equity doesn’t fail because of bad strategy. It fails when execution never becomes controlled, measurable, and real. Everyone celebrates PE transformation stories. You hear them at conferences, in case studies, on LinkedIn. The ones where a struggling business gets acquired, undergoes a dramatic transformation, and emerges leaner, faster, and worth 3–5x more than the entry price. McKinsey publishes studies on transformation success rates. Bain publishes frameworks for managing change at scale. Harvard Business Review runs features on how enterprises successfully navigated digital transformation. What you don’t hear are the quiet ones. The transformations that stopped halfway through. The ones where momentum died at month 4. The initiatives that looked perfect on a 100-day plan but collapsed under the weight of operational reality. The promised EBITDA that never materialised. The exit window closed because the business hadn’t actually changed. Based on 30 years in transformation programmes — at scale, across industries, in high-stakes environments — I’ve seen enough of these failures to know they follow a pattern. I’ve worked through post-acquisition integrations at Fortune 500 firms. I’ve run PMOs on nine-figure transformation programmes. I’ve been brought in as a turnaround officer to salvage transformations that were already failing. I’ve also been the sponsor on the PE side, looking at a struggling portfolio company and asking the hard question: why hasn’t this changed? And here’s what nobody wants to say out loud, because it’s uncomfortable and it implicates every leader who’s been through this: Most PE transformations fail not because the strategy was wrong. They fail because the execution engine never became real. The Five Silent Killers When a PE-backed transformation falters, it’s almost always one of these five things. Not all at once — but usually at least two, working together to kill momentum. What’s insidious about these failures is that they don’t manifest as dramatic breakdowns. They manifest as a slow drift. As a creeping scope. As initiatives that are technically ‘on track’ but aren’t delivering the needle-moving results they were supposed to. 1. Weak Execution Engine (The PMO That Isn’t) Here’s the dangerous assumption that disabled people make most transformations: if you build the right plan, execution will follow. It won’t. The most common transformation failure I’ve seen is a PMO that looks good on the org chart but doesn’t actually drive anything. It has meetings. It has workstreams. It has a 200-page roadmap with Gantt charts and resource allocations. It has governance tiers and escalation paths. It reports weekly status to steering committees. But it doesn’t have teeth. A weak execution engine typically exhibits these symptoms: Monthly status updates instead of weekly cadence. Transformation momentum requires constant visibility. In a monthly steering committee, too much can go wrong between meetings. Blockers that should be cleared in 2 days sit for 3 weeks. Small misses compound into big ones. A monthly rhythm is basically an admission that you’re not managing by fact — you’re managing by hope and hoping the next month’s update is better than this month’s. No single point of accountability. When a workstream misses a milestone, who owns it? If the answer isn’t crystal clear — one name, one person, one P&L — then it’s everyone’s responsibility, which in practice means nobody’s. I watched a transformation workstream on supply chain efficiency miss three successive milestones before anyone acknowledged it wasn’t happening. Seven people were listed as ‘sponsors’ for the initiative. Decisions deferred to consensus. I’ve watched transformations grind to a halt because the PMO couldn’t make a $2M decision without five rounds of stakeholder consultation. There’s an appeal to consensus — it feels inclusive. It feels safe. But by the time consensus forms across five business units with competing interests, the market has moved, and the initiative is already behind. Dashboards that don’t drive behaviour. You can have all the red/amber/green metrics you want. If they don’t lead to immediate corrective action — if a red metric doesn’t trigger an emergency decision meeting within 48 hours — then you’re just producing status reports dressed up as KPIs. The dashboard serves as a cover: ‘We tracked it closely,’ the PMO says, even though nothing actually changed in response. PMO focused on process instead of outcomes. The most dangerous transformation of PMO is one that confuses process compliance with delivery. ‘All workstreams submitted their risk registers.’ ‘Governance tiers are in place.’ ‘Change management plan is complete.’ These are process boxes. They’re not EBITDA. A transformation PMO’s job isn’t to ensure the process is perfect — it’s to ensure the business changes. The PE firms that succeed insist on a fundamentally different operating model for the execution engine. Weekly cadence — not monthly. Unambiguous ownership — one person’s name next to each initiative. Escalation paths that clear decisions in 48 hours, not 6 weeks. Dashboards that trigger action, not just reporting. An execution engine isn’t a support function — it’s the organism that keeps the transformation moving. 2. Too Many Initiatives, Zero Prioritisation A classic mistake in transformation planning: the first Value Creation Plan tries to do everything, because everything represents an opportunity. Improve margins through aggressive cost reduction across all functions. Drive growth through channel expansion, product innovation, and geographic rollout. Modernise the technology infrastructure and migrate to the cloud. Restructure talent and eliminate redundancy. Get exit-ready by creating sustainable, scalable operations. Improve customer experience and NPS. Refine the go-to-market strategy. All simultaneously. The result: thousands of people working across dozens of workstreams, nothing delivered with real impact. Small wins scattered across initiatives, but no material EBITDA impact. Teams are exhausted by complexity and context switching. Leadership is confused about what actually matters. I was brought in to salvage a transformation at a mid-market manufacturer that was struggling. The company had been PE-backed for 18 months. The transformation had identified over 40 initiatives across cost, revenue, technology, and organisational restructuring. Every business unit was running three to four ‘high-priority’ programmes. Nobody had time to focus on anything. And EBITDA