The Future of UAE Family Businesses: Platform, Not Company

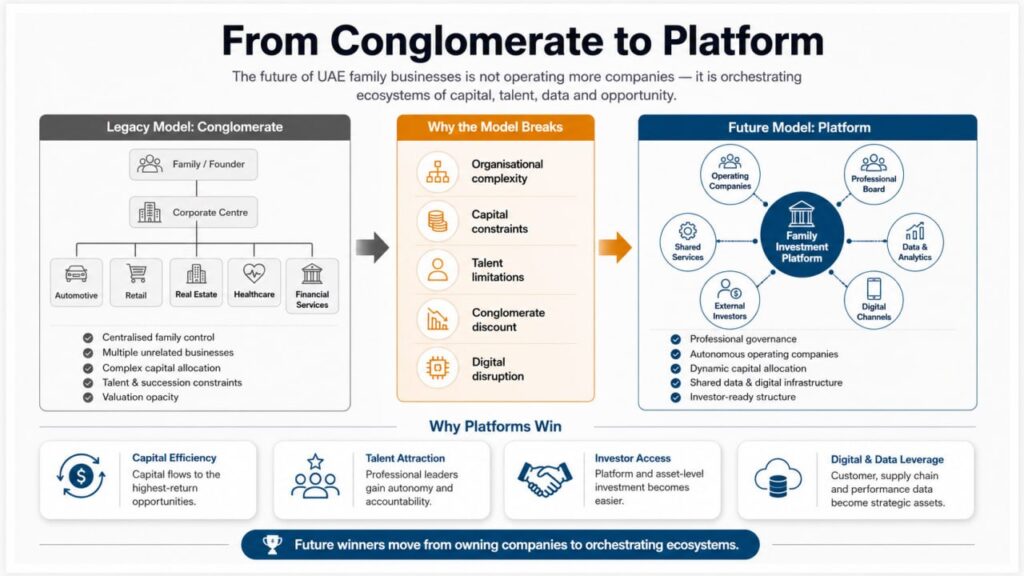

The Evolution Framework: From Conglomerate to Ecosystem The next generation of successful family businesses will not look like the family businesses that built Middle Eastern wealth over the past 50 years. They will not be organised as traditional companies—with a core business, some diversification, and a clear organisational hierarchy. They will be platforms—sophisticated ecosystems that orchestrate capital, talent, technology, and market access across multiple businesses, geographies, and sectors. This is not speculation. It is already happening. And understanding this evolution is critical for any family business seeking to remain relevant in the next decade. What the Current Model Looks Like To understand the future, let us first understand the present. The dominant family business model of the past 50 years has been the conglomerate structure. A founder builds a core business (trading, retail, distribution, manufacturing). As the business generates cash and the founder gains confidence, they diversify into adjacent or unrelated sectors. A typical family conglomerate might look like: Core Business: Automotive distribution (representing 40% of revenue)Related Diversifications: This structure worked extraordinarily well for decades. It provided: Yet this structure has constraints that are becoming increasingly visible: Organisational Complexity: Managing unrelated businesses requires different expertise. A retail leader does not necessarily understand healthcare operations. Managing all these businesses under a single corporate structure creates complexity and inefficiency. Capital Constraints: Capital deployed to one business line is unavailable for another. Optimal capital allocation across unrelated businesses is complex and imperfect. Talent Limitations: Attracting superior talent across multiple unrelated sectors is challenging. A talented healthcare executive may not want to work for an automotive distribution conglomerate. Valuation Opacity: Investors struggle to value conglomerates because they cannot readily identify which businesses generate value and which consume it. Conglomerate structures typically trade at a “conglomerate discount”—valued at less than the sum of their parts. Succession Complexity: When a founder steps back, managing multiple unrelated businesses becomes extraordinarily difficult for a single successor or set of successors. This conglomerate structure is about to give way to a different model: the platform. The Platform Model: Structure and Economics A platform, in the modern sense, is an ecosystem that creates value by connecting multiple parties (businesses, investors, service providers, customers) and enabling transactions and relationships between them. In the context of family businesses, a platform represents a shift from “the family owns multiple businesses” to “the family orchestrates an ecosystem of businesses.” The distinction is subtle but consequential. In a conglomerate model: In a platform model: This shift has several implications: Business Autonomy: Each business has a clear leader and operating model. The business is held accountable for performance. But the business operates within platform governance rather than being micromanaged centrally. Professional Management: Because businesses operate semi-autonomously, they can attract professional management talent. A talented operations executive can run a significant business within the platform without reporting through layers of family governance. Investor Engagement: A platform structure makes it easier for external investors to invest in specific businesses or in the platform itself. A PE firm might invest in a single platform business rather than acquiring the entire conglomerate. Capital Efficiency: Platform structures enable more dynamic capital allocation. Capital can be deployed toward the highest-return opportunities regardless of whether they fit the “core” business definition. Scalability: The platform structure scales more easily than conglomerate structures. As the family invests in new businesses, they add them to the platform rather than integrating them into a centralised structure. Specific Model Evolution: From Al-Futtaim to Future Platforms To make this abstract discussion concrete, consider the evolution of a group like Al-Futtaim. Current Model (Conglomerate): Evolution Toward Platform Model: This evolution enables: The Data and Analytics Layer: Core Platform Asset One critical difference between a traditional conglomerate and a modern platform is the role of data and analytics. A traditional conglomerate collects financial data (revenue, costs, profit) but may lack integrated visibility into operational data (customer behaviour, supply chain efficiency, operational quality). A modern platform goes further. It treats data as a core asset and creates visibility into: Customer Data: Who are the customers across all platform businesses? What are their purchase patterns? What additional services might they value? How can the platform cross-sell across businesses? Supply Chain Data: What are the procurement patterns across businesses? What consolidation opportunities exist? Where are inefficiencies? Operational Data: What are the key performance indicators across businesses? How do similar operations compare across different businesses? Where can best practices be shared? Financial Data: What is the true profitability of each business and each product line? How is capital deployed? Where are the highest returns? This data visibility enables: The companies that are most successful at this data integration are building a significant competitive advantage. Digital-First Operating Models: The Technology Transformation Another critical evolution in next-generation family businesses is the shift toward digital-first operating models. Traditional family businesses were built in a physical-first era. Retail meant physical stores. Distribution meant trucks and warehouses. Customer relationships meant in-person meetings. Next-generation platforms are built with digital-first approaches: Direct-to-Consumer Platforms: Rather than selling through traditional retail or distribution channels, businesses increasingly sell directly to consumers through digital platforms. This improves margins and provides direct customer data. Marketplace Models: Rather than owning inventory, some platforms are evolving toward marketplace models where they connect buyers and sellers and take a commission. This capital-lighter model is more scalable. Technology-Enabled Services: Many traditional services (retail, distribution, financial services) are being reimagined as technology-enabled services. A retailer becomes a mobile shopping app. A distributor becomes a supply chain logistics platform. Data-as-a-Service: Some platforms are discovering that the data they own (customer behaviour, supply chain patterns, market insights) can be monetised as a service. A distributor might sell supply chain visibility to suppliers. This digital transformation enables: The Investment Arm Model: Capital as the Platform The most sophisticated next-generation family businesses are evolving the investment arm as the core platform. Rather than being a back-office support function, the family office becomes the strategic centre of the platform. The investment arm: This investment-arm model has

The Silent Risk: What Happens When Nothing Changes

The Comfort of Success: A Dangerous Assumption There is a particular comfort that comes with running a successful business for decades. Markets have been kind. The founder has built something substantial. Cash flows are healthy. The customer base is loyal. Employees have been with the company for years. Suppliers know how to work with the business. The regulatory environment is stable. The business has succeeded by doing what it has always done. This success creates a particularly dangerous psychological dynamic: the assumption that continued success requires nothing more than maintaining current approaches. This assumption is understandable. It is also potentially catastrophic. Because the external environment in which family businesses operate is not static. Markets are changing. Competition is intensifying. Technology is disrupting traditional business models. Customer preferences are evolving. Regulatory frameworks are becoming more stringent. The labour market is shifting. Generational expectations are changing. Stability and unchanging operations, which were the source of past success, become the source of future decline. The Risk Landscape: What Changes and What It Means To understand the silent risk of inaction, we must examine the external environment changes that are transforming business conditions across the GCC: Market Consolidation and New Competition For decades, many family businesses operated in industries with a stable, predictable competitive landscape. The top three players remained the top three players. New competitors entered rarely and with difficulty. Margins were sustainable. This is changing. Several forces are driving market disruption: Global multinationals are increasingly comfortable operating in GCC markets. Walmart entered through Carrefour’s ownership. Amazon is building regional logistics capabilities. FMCG multinationals are improving distribution directly, reducing dependence on traditional distributors. Professional management is becoming table stakes, not a competitive advantage. Technology-enabled competitors are emerging. E-commerce platforms are consolidating retail, eating into traditional retail margins. Digital marketplaces are disintermediating traditional distribution models. FinTech platforms are competing with traditional financial services. Regional players from adjacent markets are expanding across borders. An excellent distributor from Egypt or Saudi Arabia sees an opportunity in the UAE market and enters with modern approaches and lower cost structures. Within the GCC, family businesses are consolidating, creating super-competitors with greater scale, specialised functions, and operational sophistication. The consequence: The stable competitive environment that has characterised many industries is becoming unstable. A secure market position is becoming vulnerable. A company that was the clear category leader is facing new competitors and margin pressure. A family business that assumes it will maintain its market position through existing approaches is operating from a dangerous assumption. Changing Customer Expectations Customer expectations are evolving in ways that many traditional family businesses have not fully internalised. Digital-native customers (typically younger, educated abroad, exposed to global consumer experiences) have different expectations: Traditional family businesses that excel at personal relationships and in-person service often lag in digital capabilities and omnichannel experience. A retail business that was world-class in in-store experience may be fundamentally unprepared for e-commerce competition. Similarly, B2B customer expectations are evolving. Large corporate customers increasingly demand integration with digital platforms, real-time visibility into supply chains, and data-driven reporting. A distribution company that sold through personal relationships and phone orders is competing with suppliers that offer cloud-based ordering platforms and automated fulfilment. Customers are not loyal forever, and not to traditional approaches. Loyalty is to companies that meet evolving expectations. A business that ignores these changes loses market share to more responsive competitors. Technological Disruption The pace of technology change is accelerating. Technologies that were science fiction a decade ago are now accessible and affordable: A family business that does not embrace technology will find itself unable to compete with companies that do. A manufacturing company without ERP visibility into production costs will lose margin competition to one with real-time production analytics. A retail company without e-commerce will lose market share to those with seamless digital experiences. Technology is not a nice-to-have. It is becoming table stakes. Regulatory and Compliance Evolution The GCC regulatory environment is tightening. Governments are moving toward formalisation, transparency, and standardisation in ways that were not previously required. Examples: A family business that assumes regulatory requirements will remain static is making a dangerous assumption. Compliance is evolving, and non-compliance has increasing costs. Talent Market Changes The labour market is fundamentally shifting, and this has particular implications for family businesses: Younger employees expect: Traditional family businesses that have retained employees through personal relationships, informal advancement, and family proximity are finding that this model no longer works. Superior talent is increasingly choosing to work for professional organisations with clear career paths, competitive compensation, and recognised brands over family businesses with opaque advancement and informal processes. The consequence: Family businesses are losing their best employees to more professional competitors. The institutional knowledge that was retained through employee loyalty is walking out the door. Additionally, the cost of replacement talent has increased substantially. Recruiting, training, and retaining new talent requires investment in systems, processes, and compensation that traditional family businesses may not have budgeted for. Demographic and Generational Shifts UAE demographics are changing in ways that affect family business sustainability: The founder generation that built family businesses is ageing. Many founders are approaching retirement or have already entered their 70s or 80s. The transition to the next generation is not a future event—it is a present event. The next generation has different worldviews and expectations. Many have been educated internationally and worked at multinational corporations or in startup environments. They expect professional management, clear governance, transparent decision-making, and strategic clarity. They do not want to inherit a business structured entirely around the founder’s discretion. Additionally, demographic composition in the GCC is changing. The Emirati population is growing at different rates than expatriate populations. Government policies are increasingly favouring Emiratization (employment of citizens). A family business that relies entirely on expatriate management may find regulatory expectations shifting toward citizen employment, forcing staffing changes. Capital Market Evolution The sources and costs of capital are evolving in ways that create pressure on family businesses: Traditional bank financing was the primary source of growth capital for family

From Founder-Led to System-Led: The Shift That Defines Success

The Inflexion Point: When Personal Leadership Becomes a Constraint There is a precise moment in the life of most successful family businesses when the founder confronts a fundamental question: “Can this business continue to operate as it does, or does it need to change fundamentally?” This moment typically arrives when one or more of the following conditions emerge: When any of these conditions arise, the business faces a choice: continue to operate as a founder-led entity or transform into a system-led organisation. This choice is not simply operational. It is existential because the shift from founder-led to system-led represents a fundamental transformation of how the business functions at every level. The Founder-Led System: Its Power and Its Limitations To understand why the shift is necessary, we must first appreciate what a founder-led operation enables and what it constrains. What Founder-Led Operation Enables: Speed. When a single individual makes decisions with authority and accountability, organisations can move faster than they can under consensus-driven structures. The founder can decide in a day what would take a committee weeks to debate. Agility. The founder can rapidly reorient the business in response to new information or changing conditions. There are no committees to convince, no processes to follow, no layers to navigate. The founder sees something and pivots. Efficiency. Founder-led operations can be extraordinarily efficient because they eliminate bureaucracy, duplicate oversight, and layers of approval. The founder maintains an information advantage and can allocate resources with minimal overhead. Autonomy. The founder answers to no one and maintains full discretion over strategic decisions, capital allocation, and direction. This freedom can be exhilarating and empowering. Alignment. Because the founder has built the business personally and retains full decision authority, there is perfect alignment between intent and execution. What the founder wants is what the organisation does. What Founder-Led Operation Constrains: Scale. At some point, a business becomes too large and complex for one person to understand and direct. Customer relationships exceed what one person can maintain. Supply chains become too intricate. Market dynamics become too multifaceted. The founder’s personal attention becomes a bottleneck. Complexity. As the business scales into new sectors or markets, the founder may lack expertise in those domains. A founder who succeeded in retail distribution may lack knowledge about healthcare operations or financial services. The founder’s generalist instinct, which worked at smaller scales, becomes a liability at larger scales. Continuity. A founder-led operation is inherently brittle because it is entirely dependent on the presence and capability of a single individual. If the founder is unavailable—due to illness, accident, ageing, or death—the business lacks the infrastructure to operate. Leverage. Lenders and investors are uncomfortable with founder-dependent operations because the economic value is concentrated in a single person. The founder cannot access debt markets on favourable terms or raise equity capital because any investor would be purchasing an option on the founder’s continued availability. Talent Attraction and Retention. Highly capable professionals are often reluctant to work in organisations where all authority is concentrated in a single leader. They lack a path to advancement. They have limited autonomy. They cannot build organisations or drive initiatives of their own. Superior talent often leaves founder-led organisations for more structured environments. Formal Governance. Increasingly, stakeholders (banks, government agencies, and large customers) require evidence of formalised governance, controls, and operational transparency. A founder-led organisation can only accommodate this requirement by creating formal structures, which, by definition, moves away from pure founder-led operation. Scalability of Business Model. Some business opportunities require more capital, more specialised expertise, or larger operational scale than a founder can personally direct. The opportunity to enter a new market, acquire a competitor, or launch a new business line may require organisational investment that only a system-led organisation can provide. The System-Led Paradigm: Structure, Process, and Distributed Authority A system-led organisation operates on fundamentally different principles: Decision Authority is Distributed Rather than concentrated in the founder, decision authority is distributed across organisational roles. A CFO has authority over financial decisions within defined parameters. An operations director has authority over supply chain decisions. A retail manager has authority over store-level decisions. The founder transitions from making all decisions to approving certain decisions and setting parameters within which others make decisions. This distribution of authority creates several benefits: The cost is that the founder gives up personal control over every decision. Process Replaces Intuition In founder-led organisations, processes exist to serve the founder’s intuition. In system-led organisations, processes exist to enable consistent, high-quality decision-making across the organisation in the founder’s absence. Examples: The benefit of process-driven decision-making is consistency and scalability. The cost is that decisions take longer and may lack the founder’s intuitive insight. Organisational Layers Enable Specialisation A system-led organisation typically has more organisational layers than a founder-led one. There is senior leadership (founder/CEO and C-suite executives), middle management (directors and managers), and operational staff (specialists and frontline employees). Each layer has defined responsibilities: This layering creates several benefits: The cost is that organisational layers slow down decision-making and increase overhead. Transparency and Accountability Replace Personal Trust In founder-led organisations, accountability flows from personal trust. The founder trusts key lieutenants to execute, and if they do not, the founder applies pressure or removes them. Performance management is personal. In system-led organisations, accountability flows from transparent metrics, formal performance management, and structured consequences. Employees have clear KPIs. Performance is tracked visibly. Compensation and advancement are tied to metrics. Underperformance triggers formal management processes. The benefit is consistency and fairness. The cost is reduced personal autonomy and increased scrutiny. Data and Metrics Replace Founder Intuition Founder-led organisations often lack formal reporting and metrics. The founder “feels” whether things are going well based on personal observation and informal conversation. System-led organisations implement formal reporting. Dashboards track key metrics (revenue, margin, customer acquisition, employee turnover, operational efficiency). Data is visible across the organisation. Decisions are made based on data rather than intuition. The benefit is that decisions are informed by comprehensive information. The cost is that organisations can become data-obsessed and

Why Private Equity Loves UAE Family Businesses

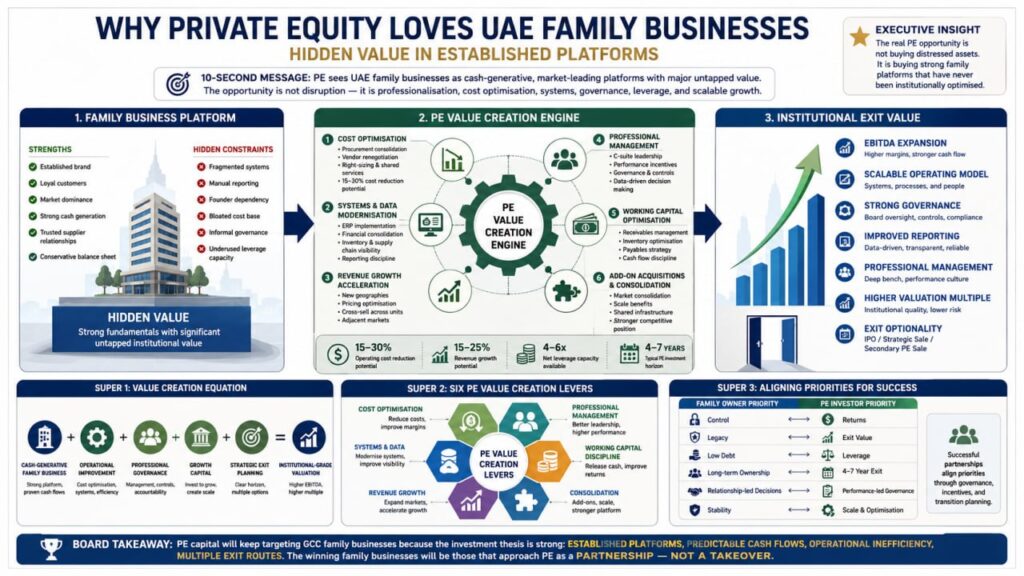

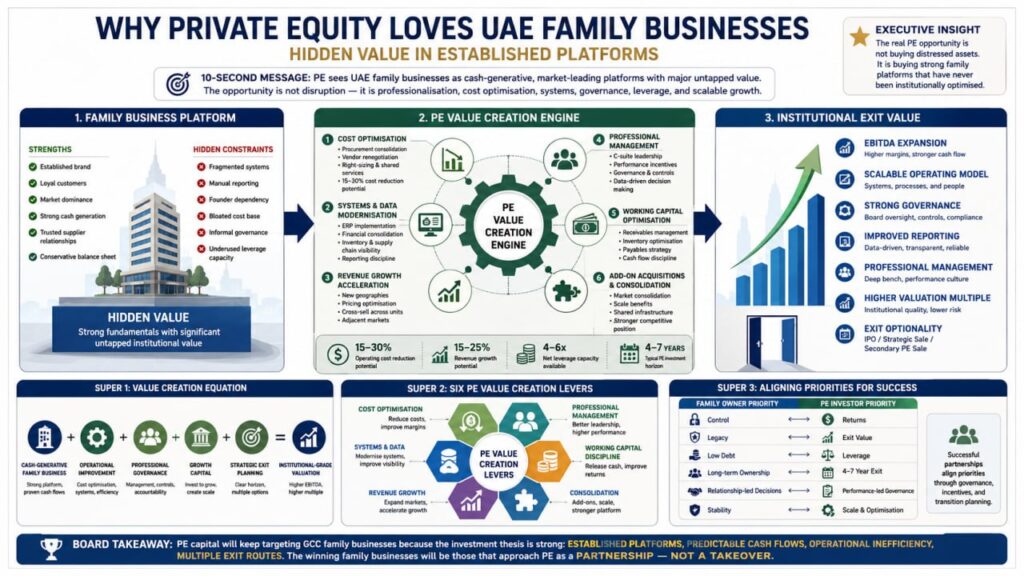

The Thesis: Hidden Value in Established Platforms If you have spent any time in the GCC private equity market over the past decade, you have witnessed a fundamental shift in investment strategy. PE firms that historically chased startups in technology hubs or infrastructure megaprojects have quietly and systematically redirected capital toward an entirely different target: established family businesses. This is not an accident or happenstance. It reflects a deliberate and strategically sound investment thesis. The thesis is simple: UAE and broader GCC family businesses represent some of the best value creation opportunities in emerging markets. They are not sexy. They do not fit the narrative of tech disruption or venture capital returns. They lack the venture-scale exit multiples that dominate headlines. Yet they offer something arguably more valuable: consistent cash generation, market dominance, operational underoptimization, and significant expansion potential—all within a stable, wealthy economy. Private equity investors have recognised what few other observers have articulated: family businesses in the GCC are platforms built to generate wealth, not to maximise economic returns or operational efficiency. The founder’s priority was not to optimise cost structure, unlock operational synergies, or implement best-in-class management practices. The founder’s priority was to generate cash and maintain family control. This creates a situation that, from a PE perspective, is extraordinarily attractive: a platform with strong fundamentals and substantial value-creation potential, sitting under a governance structure optimised for personal wealth rather than economic optimisation. The Value Creation Equation: Where PE Sees Opportunity To understand why PE finds family businesses attractive, we need to understand how PE calculates value creation. The PE model is not complex, though the execution is sophisticated. PE value creation occurs across multiple dimensions: Cost Optimisation (EBITDA Expansion) Many family businesses, particularly those in distribution, retail, logistics, or manufacturing, operate with cost structures that would be considered bloated by global standards. The reasons are often historical: A PE firm acquiring such a business typically identifies cost reduction opportunities of 15–30% of the operating cost base. For a business with $100 million in EBITDA, this could mean $15–30 million in cost reduction. These cost reductions are not achieved by cutting corners or reducing service quality. They are achieved by: The beauty of this approach, from a PE perspective, is that cost optimisation creates financial value without requiring new revenue growth. It is value creation from operational improvement alone. Structural Reorganisation and System Implementation Many family businesses operate with inefficient, manual, or incomplete operational systems. This is not necessarily a problem for a business at a certain size. It becomes a problem when the business is large enough that manual processes create bottlenecks. Common opportunities: These implementations are capital-intensive and operationally disruptive. A family business founder often resists them because they introduce cost without an obvious revenue benefit. A PE investor, however, recognises that these systems create infrastructure that enables future growth and operational leverage. Revenue Growth Acceleration Beyond cost optimisation, PE investors typically implement strategies to accelerate revenue growth: A founder-led business often deliberately constrains growth to maintain control and minimise borrowing. A PE investor, by contrast, is willing to leverage the platform to fund growth, viewing short-term financial metrics as secondary to medium-term value creation. Operational Leverage Through Professionalisation Family businesses often lack professional management structures. Decisions are made by family members who may have limited formal business training. PE investors typically bring in professional management—often at C-suite levels—to implement disciplined operational practices. This professionalisation creates value by: Working Capital Optimisation Many family businesses manage working capital conservatively, maintaining high cash buffers and extending payables cycles. PE investors often optimise working capital by: Add-On Acquisitions and Consolidation A particularly powerful PE value creation lever is acquiring smaller competitors and consolidating them into the platform. A fragmented industry suddenly becomes a consolidated platform with combined purchasing power, shared infrastructure, and expanded market reach. The Attractive Profile: What PE Looks For Not all family businesses are equally attractive to PE investors. The most attractive profiles share certain characteristics: Strong Market Position PE investors prefer platforms with established market dominance or clear competitive advantages. A retailer with an established brand and customer loyalty is more attractive than a new competitor. A distribution company with entrenched supplier relationships and customer contracts is more attractive than a transactional distributor. Consistent Cash Generation PE investors value predictable, recurring cash flows over revenue growth alone. A business that generates 20% EBITDA margins consistently is more attractive than one that grows 50% annually but is not yet profitable. Moderate Leverage Capacity PE investors favour businesses with moderate existing debt levels and strong capacity to borrow. A business already highly leveraged has limited capacity for PE-sponsored debt. A business with minimal leverage can borrow against strong cash flows, providing capital for value-creation initiatives. Experienced Management PE investors prefer to acquire from owners who have built professional management structures. If succession to a professional CEO has already occurred, the transition to PE ownership is smoother. If the business is entirely founder-dependent, the transition is riskier. Fragmented Competition or Consolidation Opportunity PE investors favour platforms that can be enhanced through add-on acquisitions. An industry in which the top player has 10–15% market share offers substantial consolidation upside. An industry where the top player holds 60% market share offers fewer opportunities. Regulatory Stability PE investors prefer businesses in industries with stable regulatory frameworks. Businesses in highly regulated sectors or those dependent on government favouritism are riskier because regulatory changes create uncertainty. Limited Dependence on a Single Customer or Vendor Businesses dependent on a single large customer or a small number of critical vendors are riskier. PE investors prefer platforms with diversified customer bases. UAE and GCC family businesses in retail, distribution, logistics, healthcare, and industrial sectors often check most of these boxes. The Attraction: Financial Engineering and Exit Strategy Beyond operational value creation, PE investors are attracted to family businesses for their favourable financial dynamics and clear exit paths. Entry Valuations Family businesses are often valued based on what the founder will accept, not on market

The Real Challenge Isn’t Growth — It’s Transition

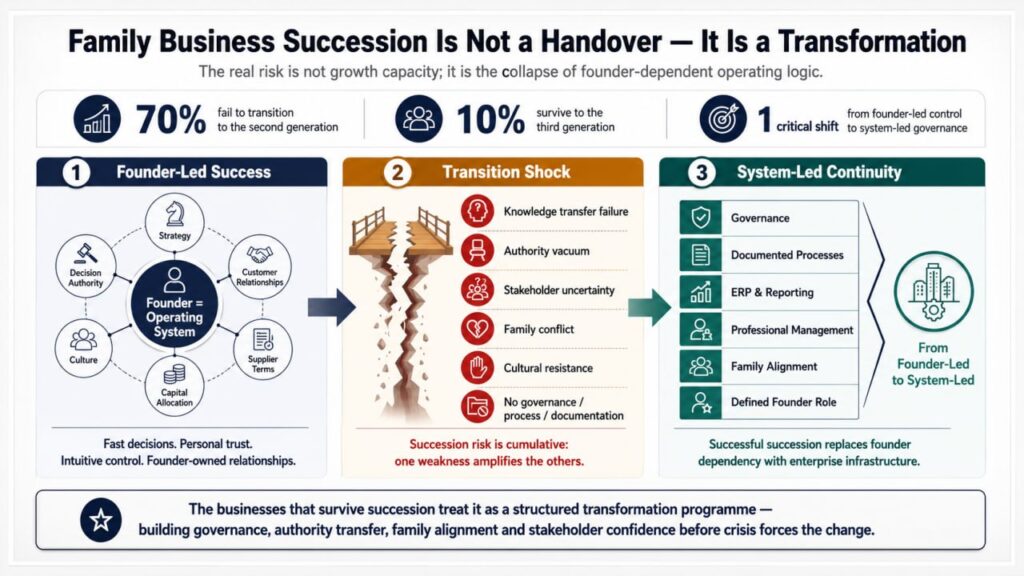

Why Family Businesses Fail at the Moment of Succession There is a paradox at the heart of family business dynamics that few outsiders truly understand: the moment of greatest strength is often the moment of greatest vulnerability. A first-generation founder has built a family business through sheer force of will, entrepreneurial vision, market timing, and relentless execution. The business is profitable. It is dominant in its market. It has successfully navigated economic cycles and competitive pressures. Cash flows are strong. Operations are understood intimately by the founder—not because they are documented, but because they exist in the founder’s mind. Then the founder faces the inevitable: ageing, retirement, mortality, or the simple desire to step back. What happens next determines whether the family business thrives for another generation or begins a slow decline into irrelevance, paralysis, or outright failure. The statistics are brutal. Approximately 70% of family businesses do not successfully transition to the second generation. Of those that do, only about 10% survive to the third generation. The United Nations estimates that across the Middle East, the situation is even more difficult, with many businesses folding entirely upon the founder’s death or departure. The prevailing assumption among external observers is that these failures stem from a lack of growth capacity, market disruption, or incompetence in the next generation. This assumption is dangerously wrong. The real reason most family business transitions fail is not about growth. It is about transformation. The Founder-Led Model: Elegant in Success, Brittle in Succession To understand why transition is so difficult, we must first understand the operating model that successful first-generation family businesses have built. The founder-led family business operates on several core principles: Founder as CEO and Chairman: The founder is not simply the leader—the founder IS the business. Strategic decisions, major capital allocation, client relationships, key vendor negotiations, and cultural authority all flow from and return to the founder. The organisational structure exists to execute the founder’s vision, not to operate independently. Information as Personal Possession: Critical business knowledge—customer relationships, supplier terms, pricing logic, capital structure, expansion plans, competitive positioning—exists in the founder’s head, not in documented systems. The founder possesses an information advantage that would be extraordinarily difficult to transfer. Decision-Making Authority as Concentrated Power: Authority is not distributed through formal structures—it is concentrated in the founder. Decisions are made quickly because there is only one decision-maker. Disagreement is resolved because the founder has final authority. Culture as Founder Personality: The organisation’s culture reflects the founder’s values, work ethic, risk tolerance, and interpersonal style. Loyalty is personal—employees work for the founder, not for the organisation. Success Metrics as Founder Intuition: Rather than formal KPIs, dashboards, and metrics, success is measured by the founder’s intuitive sense of whether things are going well. The founder “feels” when something is off, when an opportunity is emerging, or when a market is shifting. Capital Allocation as Founder Discretion: How cash flows are used—whether reinvested in operations, deployed into new business lines, distributed to family, or allocated to personal investments—is entirely the founder’s decision, often made informally. This model is extraordinarily efficient. It minimises overhead, eliminates bureaucratic decision-making, and enables rapid response to market opportunities. It has been the engine of success for countless family businesses. It is also entirely dependent on the presence and decision-making of a single individual. The Transition Trap: What Actually Changes When a founder steps back, and a successor takes over, what appears to be a simple transition—” the founder retires, the next generation takes over”—actually triggers systemic changes across every aspect of how the business operates. Knowledge Transfer Failure: The first-generation successor discovers that the information they thought they had absorbed is incomplete. They understand parts of the business they worked directly with, but they lack critical context on major client relationships, vendor negotiations, supplier dependencies, historical capital decisions, and competitive positioning. The founder’s intuitive understanding of “what we are” and “who we serve” was never explicitly articulated. Now the successor must reconstruct this knowledge while running the business. Authority Vacuum: The organisation has been trained to defer to the founder for decisions. The successor possesses formal authority but lacks the intuitive authority the founder had accumulated over decades of sound decisions. When the successor makes a decision—even a correct one—staff may second-guess it or wait to see if the founder will override it. This creates a vacuum that multiple decision-makers attempt to fill. Stakeholder Realignment: Customers, suppliers, lenders, and government counterparties built relationships with the founder rather than with the organisation. When the successor takes over, these stakeholders immediately ask: “Can this person do what the founder did?” The answer is almost always “not yet.” This creates vulnerability, allowing competitors to approach customers, suppliers to demand renegotiation of terms, and lenders to tighten credit. Strategic Direction Ambiguity: The founder’s strategic vision was often implicit—everyone knew what the business was trying to do because the founder communicated it through decisions and priorities. The successor, particularly if educated globally and exposed to diverse business models, may have a different strategic vision. The organisation suddenly faces a choice: Is the business what the founder built, or what the successor believes it should become? Cultural Friction: The successor often introduces new approaches—more formal processes, different management styles, new technology, modified compensation structures. These changes, even if beneficial, are experienced as threats by staff who benefited from the founder’s culture and approach. Family Dynamics Explosion: As the founder steps back, family members who had deferred to the founder’s authority may suddenly assert their own opinions about how the business should be run. A sibling may feel that they should have been the successor. A spouse may have different priorities. Cousins may want roles they were never considered for. The shared authority of “the founder” suddenly fragments into competing family interests. Capital Allocation Conflict: The successor may have different views on how profits should be distributed. Should capital be reinvested aggressively for growth, or should it be distributed as dividends to family members? Should the business

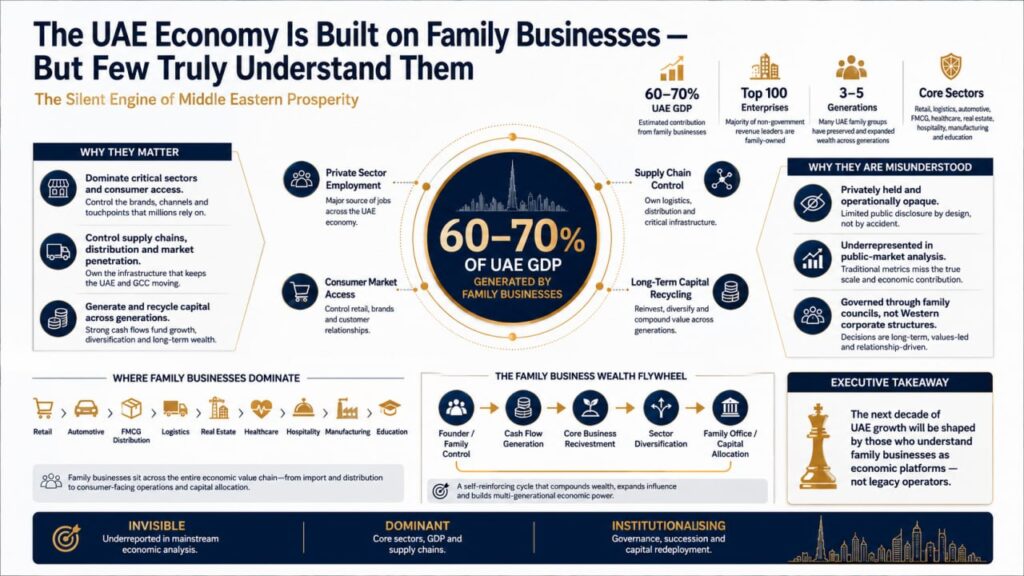

The UAE Economy Is Built on Family Businesses — But Few Truly Understand Them

The Silent Engine of Middle Eastern Prosperity When global investors, strategy consultants, and policy analysts discuss the UAE economy, the narrative is predictable and, frankly, incomplete. They cite sovereign wealth fund returns, celebrate the rise of tech startups, marvel at infrastructure megaprojects, and track foreign direct investment flows with religious precision. International media breathlessly covers the next mega-development—another skyscraper, another free zone, another billion-dirham initiative. Yet this framing misses the forest for the trees. The real economic engine of the UAE—the one that generates consistent cash flows, employs hundreds of thousands, dominates entire supply chains, and has quietly built more wealth than any government programme ever will—operates almost entirely outside the global spotlight. It is family-owned. The numbers tell a story that most observers have either overlooked or fundamentally misunderstood. Family businesses contribute between 60–70% of the UAE’s GDP. Let that sink in. Not the listed companies on the DFM or ADX. Not the foreign multinationals clustered in the Free Trade Zones. Not the government-backed mega-projects. Family-owned enterprises—many unlisted, privately held, operationally opaque to outsiders—are the foundation upon which the modern UAE economy rests. This is not hyperbole. It is an economic reality. The Scale and Scope of Family Business Dominance To appreciate the true magnitude of family business influence in the UAE, we need to move beyond GDP percentages and examine the actual architecture of economic activity. Start with retail. The dominant retailers in the UAE are family-owned. Al-Futtaim Group, one of the region’s most significant conglomerates, controls multiple retail banners across fashion, electronics, and lifestyle categories. Majid Al Futtaim operates one of the Middle East’s largest mall networks. The Al Ghurair Group maintains a massive footprint in trading, distribution, and retail. These are not niche players—they are the ecosystem operators that determine how consumers shop, what products they access, and at what price points. Carrefour’s presence in the UAE is significant, but it operates within an ecosystem designed and dominated by family businesses. Move to construction and real estate development. The major developers and contractors in the UAE are family-owned. While Emaar has gone public and become a professional corporation, the founding family maintains substantial influence. RAK Ceramics emerged from family origins. The list continues across hospitality, healthcare, and logistics. Consider logistics and distribution. This sector—unglamorous but economically vital—is almost entirely family-owned. The groups that own warehouses, manage ports, operate trucking fleets, and control the supply chain infrastructure that moves goods across the UAE and the broader GCC are family enterprises. Without them, the entire retail and manufacturing ecosystem would not function. Healthcare is another sector where family businesses have built significant empires. Private hospital networks, diagnostic centres, pharmaceutical distribution, and medical device representation—these are family-owned operations that collectively generate billions in annual revenue. Financial services also include prominent family businesses. Certain insurance brokerage networks, private equity operations, and investment vehicles are family-controlled. While conventional banking is more regulated and institutional, substantial portions of private wealth management and alternative finance pass through family office structures. The data becomes even more striking when you broaden the view. If you examine the top 100 enterprises in the UAE by revenue, the vast majority are family-owned. The concentration is particularly severe if you restrict your view to non-government entities. Public listings represent a minority of actual economic activity. The Misclassification Problem Part of why family businesses remain so invisible in mainstream economic discourse is a classification problem. When researchers, analysts, and consultants measure “the economy,” they often focus on entities that meet certain criteria: stock exchange listings, government-backed corporations, multinational operations, formal special purpose vehicles (SPVs), or regulated financial institutions. Family businesses—especially those that are entirely private, geographically concentrated, and operationally opaque—fall through the cracks of standard measurement frameworks. Moreover, many family conglomerates deliberately avoid the spotlight. They do not issue press releases about expansion plans. They do not court analyst coverage. They do not participate in earnings calls or investor presentations. They operate according to family board governance, often with minimal external disclosure. Their financial statements, if audited at all, may remain private. Their succession plans, strategic pivots, and operational challenges are handled in family meetings, not shareholder calls. This invisibility is not accidental. For decades, the prevailing view among conservative family business owners was that opacity provided protection—protection from government scrutiny, protection from competitor intelligence, protection from family disputes becoming part of the public record, and protection from the regulatory attention that comes with scale and formality. Yet this invisibility has a cost: family businesses are systemically underestimated in narratives about the UAE economy. The Sectors Where Family Business Dominance Is Absolute To move from the abstract to the concrete, let’s examine specific sectors where family business control is not just significant but essentially complete. Trading and Import/Export: The traditional import-export houses that have served as the lifeblood of UAE commerce for decades are almost universally family-owned. These trading companies represent the continuation of the historical merchant class that made Dubai and other emirates wealthy through regional commerce. They import goods, manage supply chains, manage distribution networks, and represent foreign brands across the region. The scale of these operations is often underestimated because they operate through B2B channels rather than consumer-facing ones. Automotive Distribution: The dealerships and distribution networks for major automotive brands (Mercedes, BMW, Toyota, Nissan, Hyundai) are family-owned franchises. These are extraordinarily profitable operations with recurring revenue streams from sales, servicing, spare parts, and financing. A single automotive distributor can generate hundreds of millions of dirhams in annual turnover. FMCG Distribution and Retail: While multinational FMCG companies (Procter & Gamble, Nestlé, Coca-Cola) handle manufacturing and global strategy, the actual distribution, retail presence, and consumer-facing operations in the UAE are managed through family-owned distribution networks and retail chains. Family businesses are the last-mile operators that determine market access. Hospitality and Tourism: Beyond the large international hotel chains, much of the UAE’s hospitality ecosystem—boutique hotels, tourism operators, restaurant groups, and hospitality service providers—is family-owned. Family business operations often shape the experiences of tourists and business travellers. Real Estate