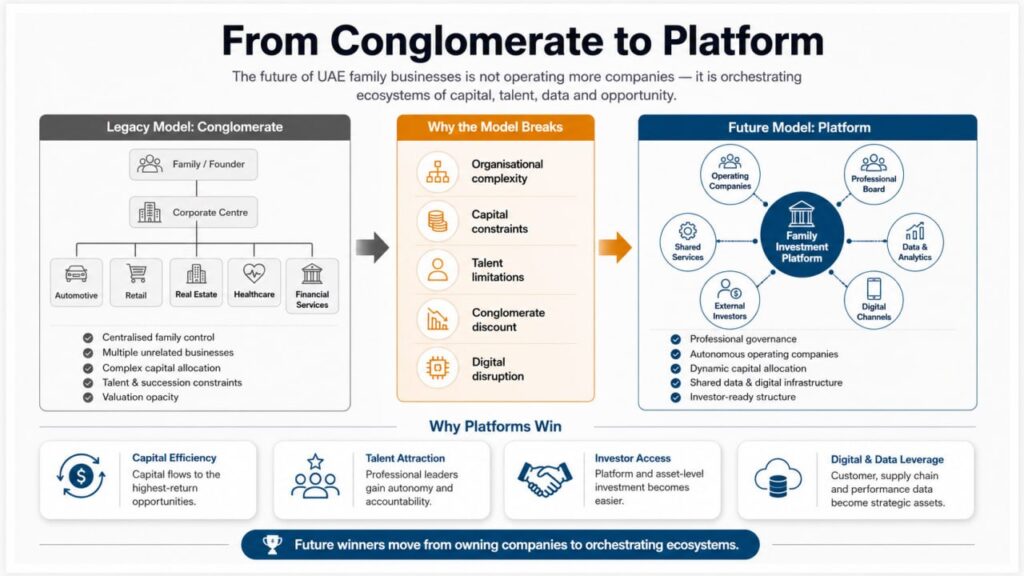

The Evolution Framework: From Conglomerate to Ecosystem

The next generation of successful family businesses will not look like the family businesses that built Middle Eastern wealth over the past 50 years.

They will not be organised as traditional companies—with a core business, some diversification, and a clear organisational hierarchy.

They will be platforms—sophisticated ecosystems that orchestrate capital, talent, technology, and market access across multiple businesses, geographies, and sectors.

This is not speculation. It is already happening. And understanding this evolution is critical for any family business seeking to remain relevant in the next decade.

What the Current Model Looks Like

To understand the future, let us first understand the present.

The dominant family business model of the past 50 years has been the conglomerate structure. A founder builds a core business (trading, retail, distribution, manufacturing). As the business generates cash and the founder gains confidence, they diversify into adjacent or unrelated sectors.

A typical family conglomerate might look like:

Core Business: Automotive distribution (representing 40% of revenue)

Related Diversifications:

- Real estate development and rental (25% of revenue)

- Retail operations (20% of revenue)

- Healthcare facilities (10% of revenue)

- Financial services/trading (5% of revenue)

This structure worked extraordinarily well for decades. It provided:

- Diversification: Revenue was not dependent on a single sector

- Capital recycling: Cash from one business funded growth in others

- Risk distribution: Downturns in one sector could be offset by growth in others

- Market power: A conglomerate with presence across multiple sectors could negotiate from positions of strength

Yet this structure has constraints that are becoming increasingly visible:

Organisational Complexity: Managing unrelated businesses requires different expertise. A retail leader does not necessarily understand healthcare operations. Managing all these businesses under a single corporate structure creates complexity and inefficiency.

Capital Constraints: Capital deployed to one business line is unavailable for another. Optimal capital allocation across unrelated businesses is complex and imperfect.

Talent Limitations: Attracting superior talent across multiple unrelated sectors is challenging. A talented healthcare executive may not want to work for an automotive distribution conglomerate.

Valuation Opacity: Investors struggle to value conglomerates because they cannot readily identify which businesses generate value and which consume it. Conglomerate structures typically trade at a “conglomerate discount”—valued at less than the sum of their parts.

Succession Complexity: When a founder steps back, managing multiple unrelated businesses becomes extraordinarily difficult for a single successor or set of successors.

This conglomerate structure is about to give way to a different model: the platform.

The Platform Model: Structure and Economics

A platform, in the modern sense, is an ecosystem that creates value by connecting multiple parties (businesses, investors, service providers, customers) and enabling transactions and relationships between them.

In the context of family businesses, a platform represents a shift from “the family owns multiple businesses” to “the family orchestrates an ecosystem of businesses.”

The distinction is subtle but consequential.

In a conglomerate model:

- The family owns and operates multiple businesses

- These businesses are connected through corporate structure and capital flows

- The centre (family office, corporate centre) manages all businesses

- Strategic decisions are made centrally

- The centre allocates capital

In a platform model:

- The family owns an investment arm that invests in and manages multiple businesses

- These businesses are connected through shared infrastructure, customer networks, and capital flows

- The centre (platform) provides governance, capital, and capabilities

- Business units have significant autonomy within platform parameters

- The platform allocates capital to businesses with the highest returns

This shift has several implications:

Business Autonomy: Each business has a clear leader and operating model. The business is held accountable for performance. But the business operates within platform governance rather than being micromanaged centrally.

Professional Management: Because businesses operate semi-autonomously, they can attract professional management talent. A talented operations executive can run a significant business within the platform without reporting through layers of family governance.

Investor Engagement: A platform structure makes it easier for external investors to invest in specific businesses or in the platform itself. A PE firm might invest in a single platform business rather than acquiring the entire conglomerate.

Capital Efficiency: Platform structures enable more dynamic capital allocation. Capital can be deployed toward the highest-return opportunities regardless of whether they fit the “core” business definition.

Scalability: The platform structure scales more easily than conglomerate structures. As the family invests in new businesses, they add them to the platform rather than integrating them into a centralised structure.

Specific Model Evolution: From Al-Futtaim to Future Platforms

To make this abstract discussion concrete, consider the evolution of a group like Al-Futtaim.

Current Model (Conglomerate):

- Central corporate headquarters manages multiple business units

- Business units span retail, automotive, real estate, and industrial

- Corporate governance is family-centred

- Capital allocation is determined centrally

Evolution Toward Platform Model:

- Create separate operating companies for each business (Al-Futtaim Retail, Al-Futtaim Automotive, Al-Futtaim Real Estate, Al-Futtaim Industrial)

- Establish an investment arm (Al-Futtaim Capital or similar) that manages the group

- Each operating company has a professional CEO and board

- Capital is deployed by the investment arm to businesses based on return expectations

- Shared services (finance, HR, IT) remain centralised but operate as service providers to business units rather than as controllers

- The family governance remains at the investment company level, not at individual business unit levels

This evolution enables:

- Business simplicity: Each operating company is simpler to understand and value

- Talent attraction: Each business can attract world-class talent by offering autonomy and clear accountability

- External capital: PE firms can invest in individual operating companies or in the investment platform

- Growth capacity: The platform can acquire new businesses without requiring them to fit a predetermined corporate structure

The Data and Analytics Layer: Core Platform Asset

One critical difference between a traditional conglomerate and a modern platform is the role of data and analytics.

A traditional conglomerate collects financial data (revenue, costs, profit) but may lack integrated visibility into operational data (customer behaviour, supply chain efficiency, operational quality).

A modern platform goes further. It treats data as a core asset and creates visibility into:

Customer Data: Who are the customers across all platform businesses? What are their purchase patterns? What additional services might they value? How can the platform cross-sell across businesses?

Supply Chain Data: What are the procurement patterns across businesses? What consolidation opportunities exist? Where are inefficiencies?

Operational Data: What are the key performance indicators across businesses? How do similar operations compare across different businesses? Where can best practices be shared?

Financial Data: What is the true profitability of each business and each product line? How is capital deployed? Where are the highest returns?

This data visibility enables:

- Portfolio optimisation: Identifying which businesses are generating value and which should be divested

- Cross-selling: Identifying customer opportunities across businesses

- Procurement leverage: Consolidating supplier relationships across businesses

- Best practice sharing: Identifying and deploying successful practices from one business to others

- Investment decisions: Making informed capital allocation decisions based on complete data

The companies that are most successful at this data integration are building a significant competitive advantage.

Digital-First Operating Models: The Technology Transformation

Another critical evolution in next-generation family businesses is the shift toward digital-first operating models.

Traditional family businesses were built in a physical-first era. Retail meant physical stores. Distribution meant trucks and warehouses. Customer relationships meant in-person meetings.

Next-generation platforms are built with digital-first approaches:

Direct-to-Consumer Platforms: Rather than selling through traditional retail or distribution channels, businesses increasingly sell directly to consumers through digital platforms. This improves margins and provides direct customer data.

Marketplace Models: Rather than owning inventory, some platforms are evolving toward marketplace models where they connect buyers and sellers and take a commission. This capital-lighter model is more scalable.

Technology-Enabled Services: Many traditional services (retail, distribution, financial services) are being reimagined as technology-enabled services. A retailer becomes a mobile shopping app. A distributor becomes a supply chain logistics platform.

Data-as-a-Service: Some platforms are discovering that the data they own (customer behaviour, supply chain patterns, market insights) can be monetised as a service. A distributor might sell supply chain visibility to suppliers.

This digital transformation enables:

- Capital efficiency: Less capital is required to scale technology-based businesses vs physical business models

- Market reach: Digital platforms can reach customers across geographies more efficiently than physical expansion

- Customer insight: Direct digital relationships provide richer customer data

- New revenue streams: Data and digital services create new monetisation opportunities

The Investment Arm Model: Capital as the Platform

The most sophisticated next-generation family businesses are evolving the investment arm as the core platform.

Rather than being a back-office support function, the family office becomes the strategic centre of the platform. The investment arm:

- Makes investment decisions about which businesses to acquire, divest, or grow

- Manages portfolio companies through professional governance structures

- Allocates capital based on return expectations and strategic fit

- Sources new investment opportunities actively rather than passively managing existing businesses

- Develops investment professionals who can evaluate and manage businesses across sectors

This investment-arm model has several advantages:

- Professional discipline: Capital allocation is based on investment returns, not founder preference

- Scalability: The model scales because it is based on professional investing, not founder effort

- External capital: Sophisticated investors (institutions, family offices, other investors) are more willing to invest in a platform managed by professional investors

- Exit capability: The platform can monetise exits at the investment level rather than at the operating company level

Groups like Chalhoub Group have evolved in this direction, with significant investment arms managing capital across multiple sectors.

The Sovereign Wealth Fund Model: The Ultimate Evolution

The most ambitious next-generation family businesses are evolving toward a sovereign wealth fund model—essentially creating mini-institutional investment platforms.

In this model:

- The family accumulates capital from operating businesses

- A professional investment team manages the capital

- The team invests across multiple sectors, geographies, and asset classes

- Some capital remains in operating businesses, but significant capital is deployed into financial investments (real estate, equity stakes, bonds, alternative investments)

- The platform becomes a multi-hundred-million or multi-billion capital allocator

This model has several characteristics:

- Scale: The platform manages capital at a scale that commands institutional respect and market power

- Diversification: Capital is deployed across diverse investments, reducing concentration risk

- Return focus: The focus is explicitly on return generation, not on operating specific businesses

- Professional management: The platform is managed by world-class investment professionals, not by the founder

- Institutional gravitas: The platform has institutional credibility and can compete with pension funds, endowments, and sovereign wealth funds

Groups like the Mubadala Development Company (which began as a family-controlled entity) have evolved toward this model, managing tens of billions of dollars in assets across diverse global investments.

The Governance Evolution: From Family Control to Professional Governance

As family businesses evolve from companies to platforms, governance must evolve accordingly.

Stage 1: Founder Control

- The founder makes all decisions

- Family members are involved informally

- Governance is minimal

Stage 2: Family Council

- The family meets formally to make decisions

- Governance structures are created but remain family-focused

- Professional management is limited

Stage 3: Family Office with Professional Board

- A professional family office manages assets and investments

- A professional board oversees major decisions

- Family has governance input, but decisions are professional

Stage 4: Institutional Governance

- The platform is governed as a professional institution

- The family retains ownership but not operational control

- Governance is indistinguishable from that of a professionally-managed institutional investor

Most next-generation platforms are evolving from Stage 2 toward Stage 3. The most sophisticated are approaching Stage 4.

This governance evolution is necessary because:

- Scale: As platforms grow, family-based decision-making becomes a constraint

- Complexity: Professional governance is required to manage complexity

- Talent: Professional managers expect professional governance structures

- Investor confidence: External investors prefer professional governance

The Convergence: From Business Families to Investment Families

The ultimate implication of this evolution is that family businesses are gradually converting from “business families” (families that operate businesses) to “investment families” (families that manage capital and investments).

This convergence is already visible:

- Families that historically made their wealth in trading are now managing diversified investment portfolios

- Families that built retail empires are now investing across multiple sectors

- Families that operated manufacturing businesses are now managing sophisticated capital allocation strategies

This shift is profound because it changes the nature of family engagement:

- From operations to strategy: Rather than managing day-to-day operations, the family focuses on capital allocation and strategic direction

- From personal relationships to professional management: Rather than founder-driven relationships, the platform relies on professional management

- From company building to wealth management: Rather than measuring success by business size, success is measured by return on capital and wealth creation

The Generational Advantage: Why Next-Generation Platforms Win

The next generation of family business leaders is uniquely positioned to drive this platform evolution because they have been educated and exposed to institutional investing, professional management, and global capital markets in ways their parents were not.

A second or third-generation family leader who studied at a top business school and worked at a PE firm or institutional asset manager brings frameworks and experiences that naturally lead toward platform models.

These next-generation leaders are often frustrated by traditional family business structures precisely because they see the potential for more professional, more efficient, more scalable models.

The family businesses that will thrive in the next 20 years are those where:

- The founder or senior generation recognises the value of platform evolution

- The next generation brings the skills and perspectives to build professional platforms

- The transition is managed as a deliberate strategic evolution, not as a crisis-driven transformation

The Positioning Advantage: Why Platform Positioning Matters

Understanding this evolution has a practical implication for current family business leaders.

If you position yourself and your business at the forefront of this evolution—moving toward platform models, professional governance, and sophisticated capital allocation—you signal to the market, investors, and your organisation that you understand the future.

You become attractive to:

- PE investors who see an opportunity to partner in platform evolution

- Professional managers who see clear career paths within a sophisticated platform

- Customers and suppliers who see a stable, professionally-managed partner

- Next-generation leaders who see an opportunity to build something ambitious and modern

Conversely, family businesses that remain stuck in traditional conglomerate models signal stagnation, limited growth potential, and vulnerability to disruption.

Conclusion: The Coming Transformation

The family businesses that will dominate the GCC and broader Middle East in 20 years will look substantially different from those that dominate today.

They will be organised as platforms, not conglomerates.

They will be managed by professional investors, not by founders.

They will be governed by institutional boards, not by family councils.

They will compete based on capital efficiency and return generation, not based on founder reputation.

They will be digital-first, data-driven, and globally connected.

The transition to this model is already underway. Some groups are leading it. Others are lagging.

For the family business leaders reading this: the question is not whether this evolution will occur. It will. The question is whether you will lead it or be left behind.

The families that proactively evolve toward platform models—that professionalise governance, attract investment talent, build digital capabilities, and create institutional structures—will generate exponentially more wealth than those that cling to traditional models.

The opportunity is extraordinary. But it requires recognising that the future of family business is not about operating more companies.

It is about orchestrating ecosystems of capital, talent, and opportunity.