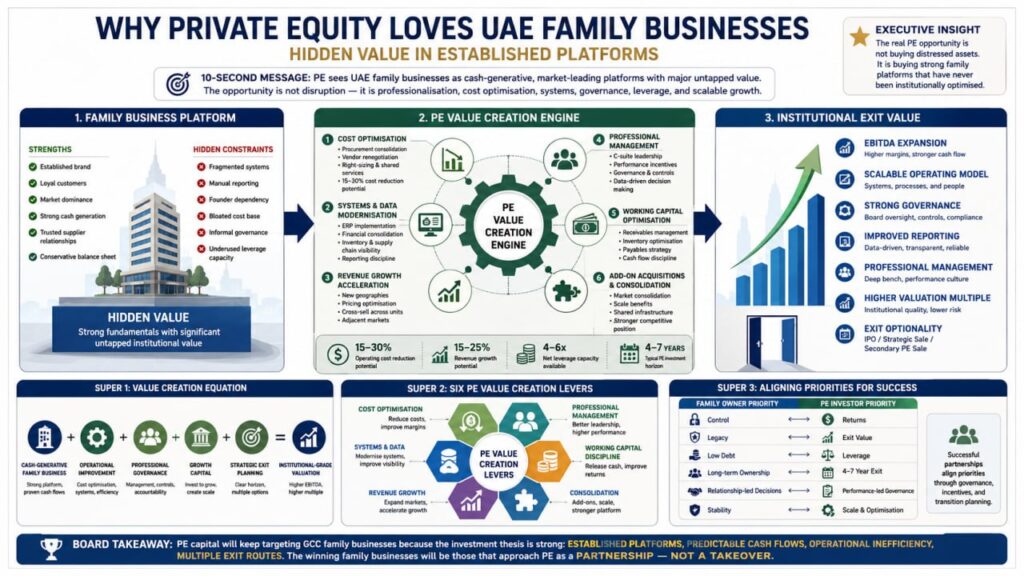

The Thesis: Hidden Value in Established Platforms

If you have spent any time in the GCC private equity market over the past decade, you have witnessed a fundamental shift in investment strategy. PE firms that historically chased startups in technology hubs or infrastructure megaprojects have quietly and systematically redirected capital toward an entirely different target: established family businesses.

This is not an accident or happenstance. It reflects a deliberate and strategically sound investment thesis.

The thesis is simple: UAE and broader GCC family businesses represent some of the best value creation opportunities in emerging markets. They are not sexy. They do not fit the narrative of tech disruption or venture capital returns. They lack the venture-scale exit multiples that dominate headlines. Yet they offer something arguably more valuable: consistent cash generation, market dominance, operational underoptimization, and significant expansion potential—all within a stable, wealthy economy.

Private equity investors have recognised what few other observers have articulated: family businesses in the GCC are platforms built to generate wealth, not to maximise economic returns or operational efficiency. The founder’s priority was not to optimise cost structure, unlock operational synergies, or implement best-in-class management practices. The founder’s priority was to generate cash and maintain family control.

This creates a situation that, from a PE perspective, is extraordinarily attractive: a platform with strong fundamentals and substantial value-creation potential, sitting under a governance structure optimised for personal wealth rather than economic optimisation.

The Value Creation Equation: Where PE Sees Opportunity

To understand why PE finds family businesses attractive, we need to understand how PE calculates value creation. The PE model is not complex, though the execution is sophisticated.

PE value creation occurs across multiple dimensions:

Cost Optimisation (EBITDA Expansion)

Many family businesses, particularly those in distribution, retail, logistics, or manufacturing, operate with cost structures that would be considered bloated by global standards. The reasons are often historical:

- Vendors are longstanding relationships, not optimised through competitive bidding

- Procurement is not centralised; purchasing happens across different business units without economies of scale

- Staff levels reflect historical hiring patterns and founder preferences, not optimal headcount

- Facilities may be maintained at premium levels for prestige rather than necessity

- Service contracts are often bespoke, not standardised

A PE firm acquiring such a business typically identifies cost reduction opportunities of 15–30% of the operating cost base. For a business with $100 million in EBITDA, this could mean $15–30 million in cost reduction.

These cost reductions are not achieved by cutting corners or reducing service quality. They are achieved by:

- Standardising procurement across multiple units

- Renegotiating vendor contracts from a position of consolidated purchasing power

- Right-sizing organisational layers that have become redundant

- Consolidating duplicate support functions

- Eliminating discretionary spending

- Optimising facilities and logistics networks

The beauty of this approach, from a PE perspective, is that cost optimisation creates financial value without requiring new revenue growth. It is value creation from operational improvement alone.

Structural Reorganisation and System Implementation

Many family businesses operate with inefficient, manual, or incomplete operational systems. This is not necessarily a problem for a business at a certain size. It becomes a problem when the business is large enough that manual processes create bottlenecks.

Common opportunities:

- Implementing integrated ERP systems where previously fragmented systems existed

- Standardising financial reporting and consolidation

- Creating supply chain visibility where opacity previously existed

- Implementing inventory management systems

- Establishing data-driven decision-making where previously intuitive decision-making prevailed

These implementations are capital-intensive and operationally disruptive. A family business founder often resists them because they introduce cost without an obvious revenue benefit. A PE investor, however, recognises that these systems create infrastructure that enables future growth and operational leverage.

Revenue Growth Acceleration

Beyond cost optimisation, PE investors typically implement strategies to accelerate revenue growth:

- Expanding geographic footprint using the established platform

- Adding new customer segments

- Cross-selling across multiple units of a conglomerate

- Entering adjacent markets

- Pricing optimisation (often increasing prices in markets where the business has a dominant position)

- Organic growth funding that a financially conservative founder may have resisted

A founder-led business often deliberately constrains growth to maintain control and minimise borrowing. A PE investor, by contrast, is willing to leverage the platform to fund growth, viewing short-term financial metrics as secondary to medium-term value creation.

Operational Leverage Through Professionalisation

Family businesses often lack professional management structures. Decisions are made by family members who may have limited formal business training. PE investors typically bring in professional management—often at C-suite levels—to implement disciplined operational practices.

This professionalisation creates value by:

- Improving decision-making quality and consistency

- Implementing performance-based incentive structures

- Reducing personal decision-making bias

- Creating organisational transparency

- Establishing accountability for operational metrics

Working Capital Optimisation

Many family businesses manage working capital conservatively, maintaining high cash buffers and extending payables cycles. PE investors often optimise working capital by:

- Accelerating receivables collection

- Optimising payables cycles

- Right-sizing inventory

- Deploying freed-up cash into value creation initiatives

Add-On Acquisitions and Consolidation

A particularly powerful PE value creation lever is acquiring smaller competitors and consolidating them into the platform. A fragmented industry suddenly becomes a consolidated platform with combined purchasing power, shared infrastructure, and expanded market reach.

The Attractive Profile: What PE Looks For

Not all family businesses are equally attractive to PE investors. The most attractive profiles share certain characteristics:

Strong Market Position

PE investors prefer platforms with established market dominance or clear competitive advantages. A retailer with an established brand and customer loyalty is more attractive than a new competitor. A distribution company with entrenched supplier relationships and customer contracts is more attractive than a transactional distributor.

Consistent Cash Generation

PE investors value predictable, recurring cash flows over revenue growth alone. A business that generates 20% EBITDA margins consistently is more attractive than one that grows 50% annually but is not yet profitable.

Moderate Leverage Capacity

PE investors favour businesses with moderate existing debt levels and strong capacity to borrow. A business already highly leveraged has limited capacity for PE-sponsored debt. A business with minimal leverage can borrow against strong cash flows, providing capital for value-creation initiatives.

Experienced Management

PE investors prefer to acquire from owners who have built professional management structures. If succession to a professional CEO has already occurred, the transition to PE ownership is smoother. If the business is entirely founder-dependent, the transition is riskier.

Fragmented Competition or Consolidation Opportunity

PE investors favour platforms that can be enhanced through add-on acquisitions. An industry in which the top player has 10–15% market share offers substantial consolidation upside. An industry where the top player holds 60% market share offers fewer opportunities.

Regulatory Stability

PE investors prefer businesses in industries with stable regulatory frameworks. Businesses in highly regulated sectors or those dependent on government favouritism are riskier because regulatory changes create uncertainty.

Limited Dependence on a Single Customer or Vendor

Businesses dependent on a single large customer or a small number of critical vendors are riskier. PE investors prefer platforms with diversified customer bases.

UAE and GCC family businesses in retail, distribution, logistics, healthcare, and industrial sectors often check most of these boxes.

The Attraction: Financial Engineering and Exit Strategy

Beyond operational value creation, PE investors are attracted to family businesses for their favourable financial dynamics and clear exit paths.

Entry Valuations

Family businesses are often valued based on what the founder will accept, not on market comparables. A founder may be satisfied with an 8–10x EBITDA valuation because they have not been exposed to institutional valuations and are motivated by liquidity for personal reasons (retirement, diversification, family dynamics), not by maximising valuation.

Professional equity investors, by contrast, scrutinise enterprise value closely. There is often a gap between what a founder will accept and what an institutional acquirer would pay.

Leverage Capacity

PE investors can typically leverage a platform at 4–6x net leverage, deploying borrowed capital to partially fund the acquisition while preserving equity return potential. A founder-led business, being conservative, may have carried minimal debt. The platform suddenly has significant leverage capacity.

Exit Timing and Optionality

PE investors have explicit investment horizons (typically 4–7 years) and multiple exit pathways:

- IPO (for large, professional platforms)

- Strategic sale to a larger corporation

- Sale to another PE firm

- Dividend recapitalisation (returning cash to investors mid-cycle)

- Sales of add-on acquisitions

These exit options are not available to a family business owner, who often must choose between remaining in the business indefinitely and finding a buyer.

The Tension: Alignment, Speed, and Control

Yet the relationship between PE and family business owners is inherently fraught because fundamental values and priorities often diverge.

Time Horizon Mismatch

PE investors operate on a 4–7 year investment cycle. Their objective is to maximise exit value at the end of that period. Family business owners, by contrast, often view the business as a multi-generational wealth vehicle. A decision that is optimal for exit value in year 5 may be suboptimal for the business’s long-term sustainability.

Example: A PE investor might sell off or divest a profitable division that does not fit the platform’s strategic focus, deploying the proceeds into higher-return businesses. The family owner might have wanted to retain that division because it serves the family’s employment needs or represents a business the founder built personally.

Debt Tolerance Differences

PE investors are comfortable with high leverage (4–6x net debt) if it enables return generation. Family business owners are often uncomfortable with high debt because it creates risk that the family has spent generations avoiding.

Dividend vs. Growth

PE investors typically plan for dividend distributions in years 2–4 of the investment, returning capital to investors ahead of exit. Family owners may prefer to reinvest profits for organic growth.

Operational Approach

PE investors typically implement professional management, standardised processes, and financial discipline. Family owners often prefer autonomy, flexibility, and the continuation of established approaches.

Exit Strategy

PE investors have clear exit targets and timelines. They are managing investor expectations and return thresholds. Family owners may not have an exit in mind and may become reluctant to sell even at attractive valuations.

Strategic Direction

A PE investor may direct aggressive expansion, geographic rollout, or consolidation. A family owner may prefer a slower, more controlled approach.

These tensions are not incidental—they are fundamental. They arise because PE and family ownership represent distinct optimisation functions.

The Deal Structures That Work

Successful PE investments in family businesses typically employ deal structures that attempt to bridge these tensions:

Founder/Family Retention

Rather than removing the founder or family ownership entirely, successful PE deals often retain the founder in an advisory role or as a significant minority stakeholder. This preserves founder-incentive alignment while bringing in PE capital and operational expertise.

Earnouts and Performance-Based Consideration

Rather than paying all consideration at closing, many deals use earnouts—additional payments based on the achievement of specific operational or financial milestones. This aligns family and PE incentives and ensures the family owner is motivated to support the transition.

Multiple Classes of Shares

Some structures create different share classes with different rights. The family may retain special governance rights or veto rights on certain decisions, while PE holds common equity and management control.

Founder Continuation Agreement

Rather than expecting immediate departure, successful deals often include founder/family employment agreements that allow them to continue in their operational roles for a defined period (often 2–3 years), with clear role expectations and transition plans.

Management Incentive Plans

Professional managers and key employees often receive equity stakes and performance-based incentives aligned with PE return targets.

The Middle East PE Ecosystem

The UAE and GCC PE market has evolved substantially over the past decade. Several major PE firms have established dedicated practices focused on acquisitions of established family businesses:

Global PE Firms: International PE firms have increasingly deployed capital in the GCC, recognising both the family-business opportunity and access to growth and capital available through Gulf sovereign wealth.

Regional PE Firms: Locally based PE firms have a better understanding of family business dynamics, regulatory environments, and cultural norms. Many have established significant track records in acquiring and operating family businesses.

Family Offices: Some large family groups have established private equity arms to acquire and operate other family businesses.

This ecosystem has created a robust market for family business acquisitions. A family business owner seeking to monetise part or all of their stake has multiple options and can engage in a competitive process to maximise the valuation.

The Case for Partnership: When PE Works for Family Businesses

The most successful PE-family business partnerships share several characteristics:

- Clarity on Value Creation Plan: Both parties understand what operational improvements will be implemented and how they will be executed.

- Family Involvement in Strategy: Rather than imposing a strategy, PE and family jointly develop the forward plan.

- Professional Management Complement: Professional managers brought in to execute operational improvements complement, rather than replace, experienced family managers.

- Aligned Metrics: PE and family align on what constitutes success—not just financial returns, but also business sustainability, employee welfare, and stakeholder relationships.

- Clear Governance: The board and decision-making authority are explicitly defined, with family representation and professional operators both present.

- Founder Transition Plan: If the founder is ageing or planning to step back, the transition is explicitly planned as part of the PE investment.

Conclusion: The Opportunity and the Risk

For family business owners, PE investment represents both opportunity and risk.

The opportunity is that PE brings capital, operational expertise, and proven value creation frameworks. A family business that might grow 5–10% organically under founder leadership might achieve 15–25% growth under PE ownership, with improved operational efficiency and expanded market reach.

The risk is that PE optimisation focuses on maximising exit value, which may not align with family priorities such as wealth preservation, multi-generational ownership, or business autonomy.

The family businesses that succeed with PE are those where:

- The family is clear about its objectives (partial or full exit, capital deployment, growth acceleration)

- The family carefully evaluates PE firm partners to find alignment on values and approach

- The family maintains governance representation and strategic input

- The transition is managed as a partnership, not a takeover

PE capital will continue to flow into GCC family businesses because the investment thesis is sound and the market opportunity is substantial. The question for family business owners is not whether PE will come knocking—increasingly, it will. The question is whether the family will approach PE with clarity about objectives and within a framework of partnership.