The Silent Engine of Middle Eastern Prosperity

When global investors, strategy consultants, and policy analysts discuss the UAE economy, the narrative is predictable and, frankly, incomplete. They cite sovereign wealth fund returns, celebrate the rise of tech startups, marvel at infrastructure megaprojects, and track foreign direct investment flows with religious precision. International media breathlessly covers the next mega-development—another skyscraper, another free zone, another billion-dirham initiative.

Yet this framing misses the forest for the trees.

The real economic engine of the UAE—the one that generates consistent cash flows, employs hundreds of thousands, dominates entire supply chains, and has quietly built more wealth than any government programme ever will—operates almost entirely outside the global spotlight. It is family-owned.

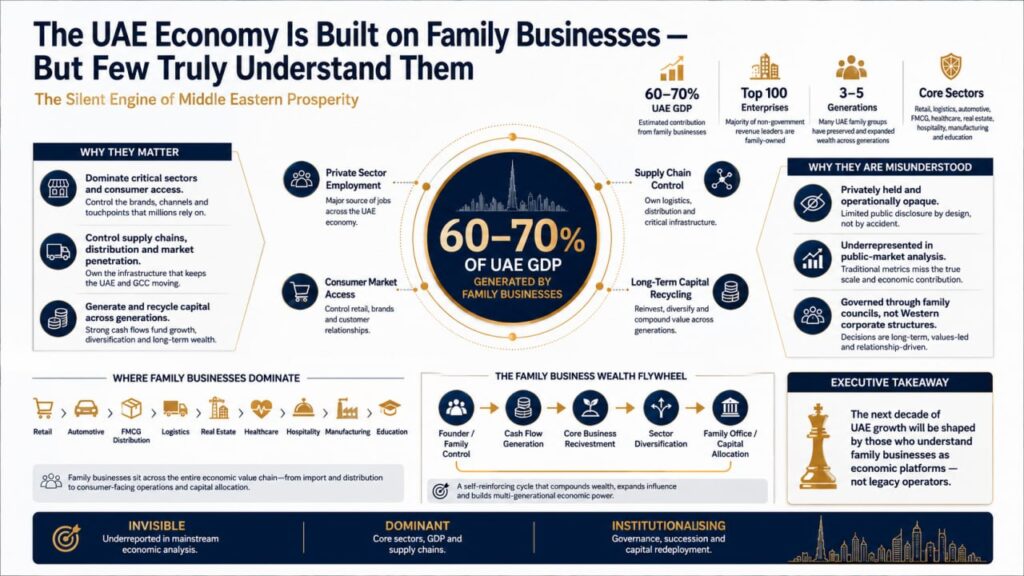

The numbers tell a story that most observers have either overlooked or fundamentally misunderstood. Family businesses contribute between 60–70% of the UAE’s GDP. Let that sink in. Not the listed companies on the DFM or ADX. Not the foreign multinationals clustered in the Free Trade Zones. Not the government-backed mega-projects. Family-owned enterprises—many unlisted, privately held, operationally opaque to outsiders—are the foundation upon which the modern UAE economy rests.

This is not hyperbole. It is an economic reality.

The Scale and Scope of Family Business Dominance

To appreciate the true magnitude of family business influence in the UAE, we need to move beyond GDP percentages and examine the actual architecture of economic activity.

Start with retail. The dominant retailers in the UAE are family-owned. Al-Futtaim Group, one of the region’s most significant conglomerates, controls multiple retail banners across fashion, electronics, and lifestyle categories. Majid Al Futtaim operates one of the Middle East’s largest mall networks. The Al Ghurair Group maintains a massive footprint in trading, distribution, and retail. These are not niche players—they are the ecosystem operators that determine how consumers shop, what products they access, and at what price points. Carrefour’s presence in the UAE is significant, but it operates within an ecosystem designed and dominated by family businesses.

Move to construction and real estate development. The major developers and contractors in the UAE are family-owned. While Emaar has gone public and become a professional corporation, the founding family maintains substantial influence. RAK Ceramics emerged from family origins. The list continues across hospitality, healthcare, and logistics.

Consider logistics and distribution. This sector—unglamorous but economically vital—is almost entirely family-owned. The groups that own warehouses, manage ports, operate trucking fleets, and control the supply chain infrastructure that moves goods across the UAE and the broader GCC are family enterprises. Without them, the entire retail and manufacturing ecosystem would not function.

Healthcare is another sector where family businesses have built significant empires. Private hospital networks, diagnostic centres, pharmaceutical distribution, and medical device representation—these are family-owned operations that collectively generate billions in annual revenue.

Financial services also include prominent family businesses. Certain insurance brokerage networks, private equity operations, and investment vehicles are family-controlled. While conventional banking is more regulated and institutional, substantial portions of private wealth management and alternative finance pass through family office structures.

The data becomes even more striking when you broaden the view. If you examine the top 100 enterprises in the UAE by revenue, the vast majority are family-owned. The concentration is particularly severe if you restrict your view to non-government entities. Public listings represent a minority of actual economic activity.

The Misclassification Problem

Part of why family businesses remain so invisible in mainstream economic discourse is a classification problem. When researchers, analysts, and consultants measure “the economy,” they often focus on entities that meet certain criteria: stock exchange listings, government-backed corporations, multinational operations, formal special purpose vehicles (SPVs), or regulated financial institutions. Family businesses—especially those that are entirely private, geographically concentrated, and operationally opaque—fall through the cracks of standard measurement frameworks.

Moreover, many family conglomerates deliberately avoid the spotlight. They do not issue press releases about expansion plans. They do not court analyst coverage. They do not participate in earnings calls or investor presentations. They operate according to family board governance, often with minimal external disclosure. Their financial statements, if audited at all, may remain private. Their succession plans, strategic pivots, and operational challenges are handled in family meetings, not shareholder calls.

This invisibility is not accidental. For decades, the prevailing view among conservative family business owners was that opacity provided protection—protection from government scrutiny, protection from competitor intelligence, protection from family disputes becoming part of the public record, and protection from the regulatory attention that comes with scale and formality.

Yet this invisibility has a cost: family businesses are systemically underestimated in narratives about the UAE economy.

The Sectors Where Family Business Dominance Is Absolute

To move from the abstract to the concrete, let’s examine specific sectors where family business control is not just significant but essentially complete.

Trading and Import/Export: The traditional import-export houses that have served as the lifeblood of UAE commerce for decades are almost universally family-owned. These trading companies represent the continuation of the historical merchant class that made Dubai and other emirates wealthy through regional commerce. They import goods, manage supply chains, manage distribution networks, and represent foreign brands across the region. The scale of these operations is often underestimated because they operate through B2B channels rather than consumer-facing ones.

Automotive Distribution: The dealerships and distribution networks for major automotive brands (Mercedes, BMW, Toyota, Nissan, Hyundai) are family-owned franchises. These are extraordinarily profitable operations with recurring revenue streams from sales, servicing, spare parts, and financing. A single automotive distributor can generate hundreds of millions of dirhams in annual turnover.

FMCG Distribution and Retail: While multinational FMCG companies (Procter & Gamble, Nestlé, Coca-Cola) handle manufacturing and global strategy, the actual distribution, retail presence, and consumer-facing operations in the UAE are managed through family-owned distribution networks and retail chains. Family businesses are the last-mile operators that determine market access.

Hospitality and Tourism: Beyond the large international hotel chains, much of the UAE’s hospitality ecosystem—boutique hotels, tourism operators, restaurant groups, and hospitality service providers—is family-owned. Family business operations often shape the experiences of tourists and business travellers.

Real Estate and Property Management: While mega-projects dominate headlines, the actual rental property management, secondary real estate development, and property services sector is substantially family-controlled. Thousands of family investors own commercial and residential portfolios and have created service businesses focused on property management.

Manufacturing: The UAE has a significant manufacturing base. Many industrial companies—from metal fabrication to food processing to chemicals—are family-owned. These are capital-intensive, operationally complex businesses built over decades.

Education and Skill Development: Private educational institutions, training centres, and educational services are frequently family-owned ventures.

The pattern across sectors is consistent: wherever there is consumer access, supply chain control, market penetration, or established customer relationships, family businesses operate at scale.

The Multi-Generational Wealth Accumulation Model

What makes UAE family businesses particularly significant—and worth serious study—is that many have successfully accumulated and retained wealth across multiple generations. This is exceptionally rare.

Globally, approximately 70% of family businesses do not survive the transition from the founder to the second generation. Fewer than 10% survive to the third generation. Yet the UAE has produced numerous examples of family conglomerates that have not only survived but thrived across three, four, and even five generations.

The Al Futtaim Group, for example, traces its origins back to the early 20th century. It has evolved from a trading house into a diversified conglomerate operating across retail, automotive, real estate, and industrial sectors. The Al Ghurair Group similarly represents multi-generational wealth preservation and expansion. Groups like Majid Al Futtaim have navigated transitions while maintaining family control.

This longevity is not accidental. It reflects several enabling factors specific to the UAE context:

Regulatory Flexibility: The UAE’s regulatory environment, while increasingly stringent, has historically allowed significant latitude in corporate governance structures, ownership continuity, and succession planning. Family businesses have not faced the same pressure toward public listing or institutional structure that might exist in more regulated economies.

Wealth Concentration Laws: Unlike some jurisdictions, the UAE has not historically imposed severe wealth taxes or inheritance taxes that would fragment family holdings across generations. This has made intergenerational wealth preservation economically viable.

Access to Capital: Successful family businesses have typically accumulated sufficient internal cash flows to self-fund growth. They have not needed to access public markets or institutional financing in ways that would dilute control.

Protected Markets: In many sectors, family businesses benefit from established relationships with government procurement processes, import duties that protect local operators, and regulatory frameworks that disadvantage foreign competitors or impose requirements that family businesses can navigate more flexibly.

Labour Access: The UAE’s visa and labour market frameworks have enabled family businesses to maintain consistency in operational management and technical expertise by sponsoring long-serving expatriate executives and specialists.

These factors, taken together, have created an environment in which family businesses can achieve scale and longevity at a genuinely exceptional rate by global standards.

The Capital Generation Model

A critical and underappreciated aspect of UAE family businesses is their role as engines of capital generation—not just for themselves but for broader regional economic activity.

Successful family businesses generate extraordinary cash flows. A profitable automotive distributor might generate 10–15% net margins on billions in turnover. A real estate company with established portfolios generates recurring rent-plus-appreciation returns. A retail network operating in a growing economy compounds its returns annually.

These cash flows have historically been retained within family structures and recirculated through several channels:

Reinvestment in Core Business: Many family businesses have systematically expanded their primary operations by reinvesting accumulated cash into additional geographic markets, product lines, or operational scale within their existing sectors.

Diversification into New Sectors: As family businesses accumulate capital, they expand into adjacent and then unrelated sectors. A trading house becomes a retailer. A retailer becomes a real estate developer. A real estate developer becomes an investor in the hospitality industry. This diversification is a natural response to capital accumulation and risk management.

Real Estate Acquisition: Family businesses have historically deployed excess capital into real estate ownership—both for operational purposes (facilities, warehouses, retail space) and as investment vehicles. Real estate has provided both operational efficiency and capital appreciation.

Equity Investments: Successful family businesses have used accumulated capital to acquire stakes in other companies, create venture investments, and establish family offices that manage diversified portfolios.

Financing and Lending: Some family businesses have evolved into quasi-financial entities, providing financing to suppliers, customers, and other operators within their ecosystem—thereby generating additional returns.

This capital recycling has made family businesses not just economic operators but also capital allocators on a scale that rivals that of institutional investors.

The Governance Reality

Understanding the true structure of UAE family businesses requires acknowledging the governance realities that differ substantially from Western corporate norms.

Many large UAE family businesses operate without formal boards of directors in the conventional sense. Decision-making authority rests with senior family members—often the founder or founding generation, sometimes transitioning to the next generation. Major decisions are made in family councils, not board meetings. Information flows through family networks, not formal organisational hierarchies.

This governance model has significant implications:

Speed of Decision-Making: Family-controlled businesses can move faster than institutional corporations because decisions do not require committee approval, formal documentation, or external stakeholder consent. A family can decide to exit a market, acquire a competitor, or pivot strategy in days, not months.

Capital Allocation: Capital is allocated based on family priorities rather than shareholder maximisation. This can mean sustained investment in unprofitable divisions if they serve family objectives, or rapid divestment from profitable ones if family priorities shift.

Talent Management: Key roles are often filled by family members, creating concerns about competency and meritocracy. Simultaneously, long-serving non-family executives develop extraordinary institutional knowledge and loyalty.

Succession Planning: Succession is a family matter, not a corporate governance process. The implications can be positive (family unity, preservation of values) or catastrophic (family conflict, organisational paralysis).

Risk Management: Practices are often informal. Major risks may not be formally assessed, documented, or mitigated. Conversely, family leadership may have an intuitive understanding of market risks that formal frameworks miss.

Financial Transparency: Reporting standards vary widely. Some family businesses maintain rigorous auditing standards; others report minimally.

This governance reality is neither inherently superior nor inferior to institutional corporate governance—it is simply different. And it is the governance reality that shapes most economic activity in the UAE.

The Future Implications

The dominance of family businesses in the UAE economy has several strategic implications that deserve serious consideration:

Economic Resilience: The distributed nature of family business ownership means that economic risk is dispersed across hundreds of independent operators. If one family business fails, the broader economy absorbs the impact differently than if failure were concentrated in large institutional corporations.

Growth Constraints: Many family businesses face growth constraints imposed by family capacity, capital availability, and risk tolerance. The evolution of these constraints will shape the future economic trajectory.

Institutional Evolution: As family businesses scale and professionalise, many are introducing board structures, professional management layers, and institutional governance mechanisms. This institutional evolution will reshape how the UAE economy operates.

Capital Availability: As family businesses accumulate capital and evolve investment capabilities, they become alternative sources of capital for entrepreneurship, infrastructure, and regional development—competing with or complementing government and institutional sources.

Regulatory Adaptation: Government policy around family business governance, disclosure, taxation, and succession will influence how these enterprises evolve.

Conclusion: The Invisible Foundation

The UAE economy is built on family businesses. This is not a poetic observation—it is an economic fact. These enterprises generate the majority of economic output, employ the majority of private sector workers, control the majority of supply chains, and determine consumer access to products and services across most sectors.

The invisibility of family businesses in mainstream economic analysis reflects a measurement and classification gap, not an absence of economic significance. Those who seek to understand the UAE economy—whether as investors, policymakers, executives, or strategists—must move beyond government statistics and public listings and examine the family business ecosystem that quietly generates the bulk of regional wealth.

The winners in the coming decade will be those who understand family businesses not as legacy players clinging to outdated models, but as sophisticated economic operators managing multibillion-dirham enterprises with capabilities that rival those of much larger institutional corporations.

The question is not whether family businesses matter in the UAE economy. They unmistakably do.

The question is: Who will be the first to understand them truly?